Here’s the video version of the article:

Summary

- The big runup in the dollar that began in June of 2021 is faltering. We took a look at what factors drove the dollar higher, why it’s now weakening and where it’s headed in the next 6-12 months.

- The dollar’s rise was driven by investors seeking safe haven amidst Europe’s energy crisis and China’s weakening economy, as well as the Fed aggressively hiking interest rates in the U.S.

- Recent dollar weakening has to do with a deceleration in U.S. inflation and in interest rates, an abundance of natural gas in Europe and the loosening of Covid restrictions in China.

- As a result, we assume a reversion of the uncertainty that’s plagued Europe and China, alongside falling U.S. rates. That’s a powerful confluence that will put pressure on the dollar.

- Given our views, we expect the dollar to fall 8% in the next 12 months. In a follow-up article we’ll assess how to position from the decline, as well as the implications for our model portfolio.

The Dollar: Breaking Down

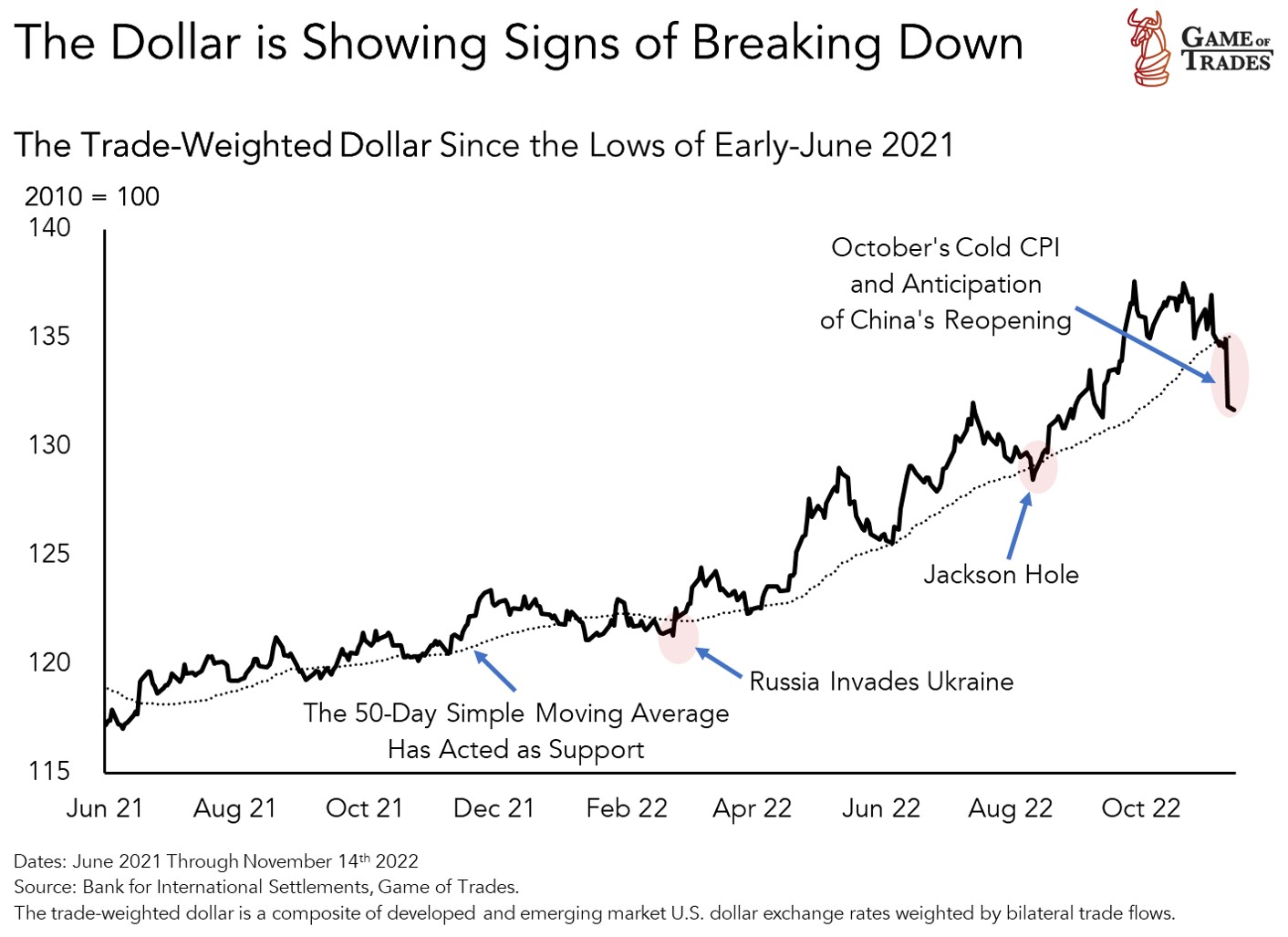

Following a relentless rise since June of 2021, the almighty dollar has been struggling lately. It’s seen a big break down as shown in the chart below, triggered by October’s cold CPI reading and anticipation of China loosening its strict Covid restrictions and reopening its economy. When referring to the dollar, in our work we prefer to use the trade-weighted version, a measure of the U.S. currency when benchmarked against a group of both developed and emerging market ones.[1]

As we mentioned in our last update on the dollar back in mid-August, we’ve had a negative bias on the greenback, but not enough for a table-pounding short bet. A couple of weeks ago, however, we positioned ourselves to take advantage of a potential reversal in the greenback by adding a 5% allocation of German small-caps to our model portfolio. That’s a group of stocks that’s highly-sensitive to moves in the euro, benefiting when it strengthens against the dollar. We’ve also had a roughly 5% allocation of Bitcoin in our portfolio as a levered bet on rising stocks and dollar weakening. As we’ve shown in prior research, the dollar is one of the big macro drivers of the digital currency.

In this research, we update our view on the dollar, reviewing what drove it higher over the last year-and-a-half, what’s causing the recent weakness, and where we see it headed in the next 6-12 months. We believe the dollar will see a 8% drop from today’s levels over that time horizon. That implies a meaningful reversal from the 12% appreciation it’s seen since June of 2021. Although our conviction level for a weaker dollar has increased, we’re not calling an end to the post-Covid dollar bull run. That’s a question for another day.

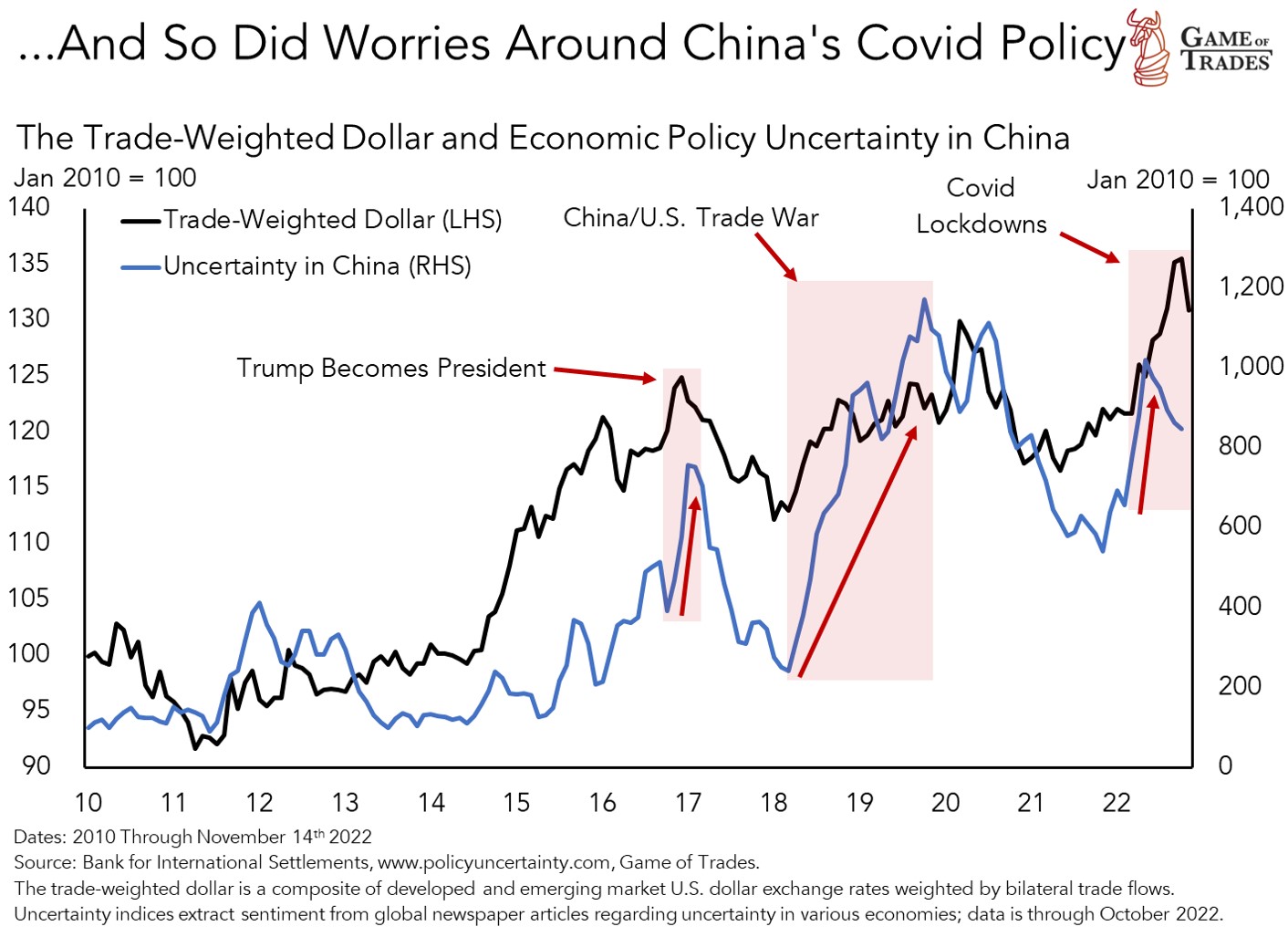

What Drove the Dollar’s Rise of the Last 1.5 Years: Europe’s Energy Crisis, China’s Covid-Zero Policy and an Aggressive Fed

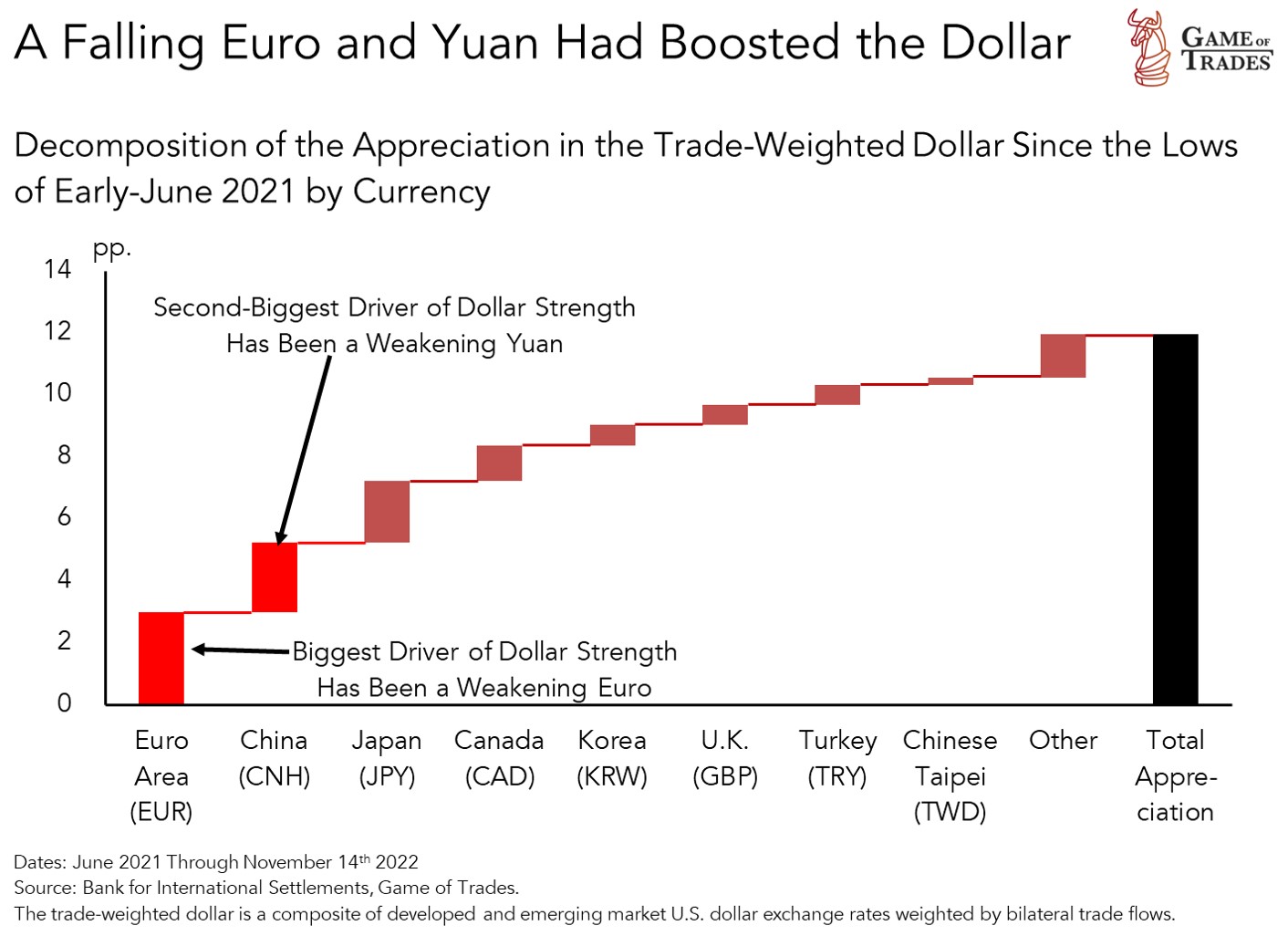

The massive dollar upcycle that began in June of last year has been driven by weakness in the euro and in the Chinese yuan, as shown below. In fact, close to half of the dollar’s 12% appreciation since then was driven by depreciation of those two currencies relative to the dollar. As a result, the rise in the dollar tells a story of headwinds facing Europe and China, two global economic powerhouses. Weakness in the Japanese yen has been a close contender, given the Bank of Japan’s continued loose monetary policy.

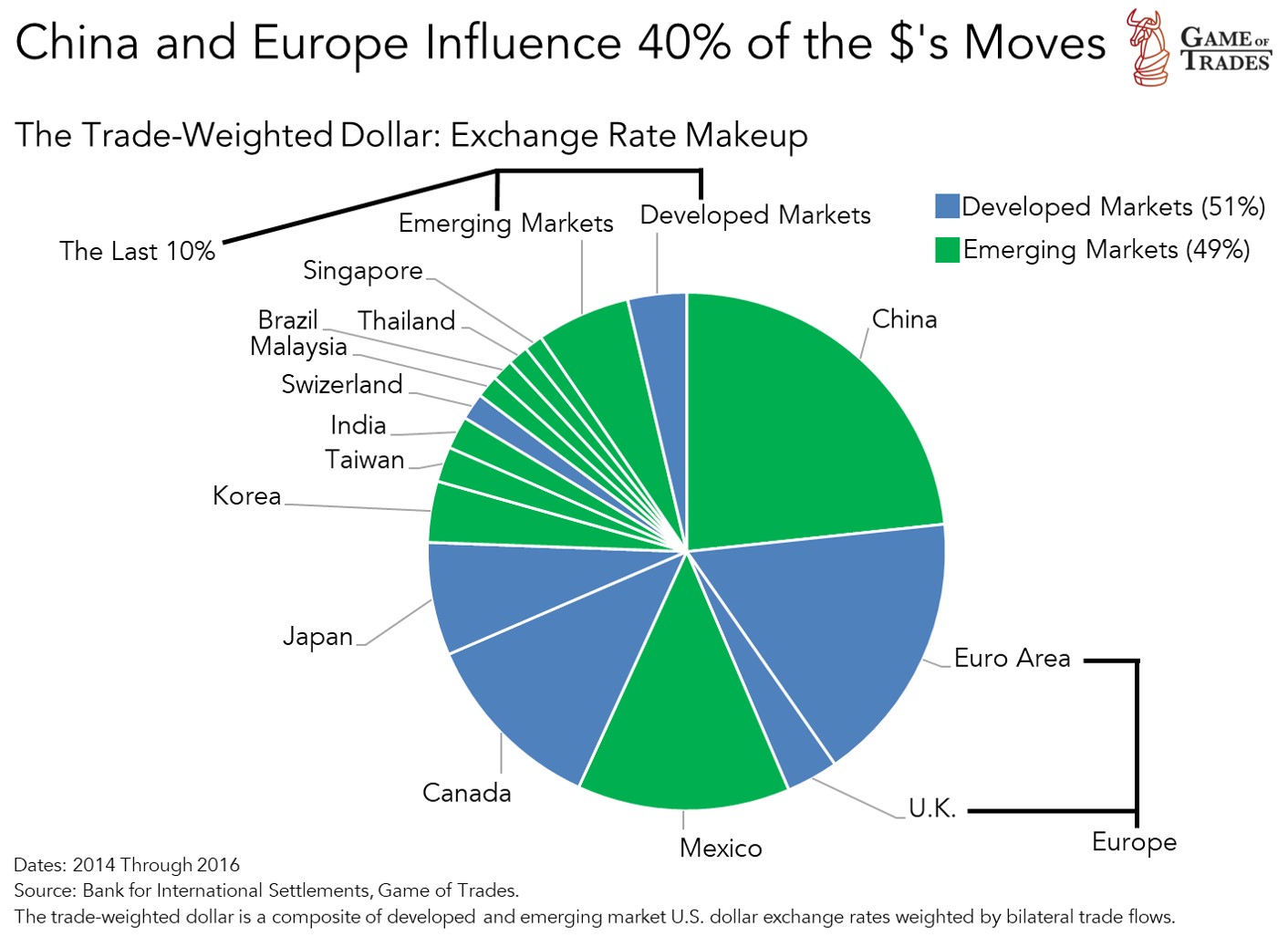

Moves in the euro and the yuan make a big impact on the trade-weighted dollar given those economies trade a lot with the U.S. (i.e., exports + imports). That gives them large weightings in its construction, comprising roughly 40% of its makeup. We can see a detailed breakout of the composition of the trade-weighted dollar by geography in the chart below. U.S. dollar exchange rates with emerging market economies, like those of the Chinese yuan and Mexican peso, are about just as important as developed ones like the euro, pound and yen. There’s a 50/50 split.

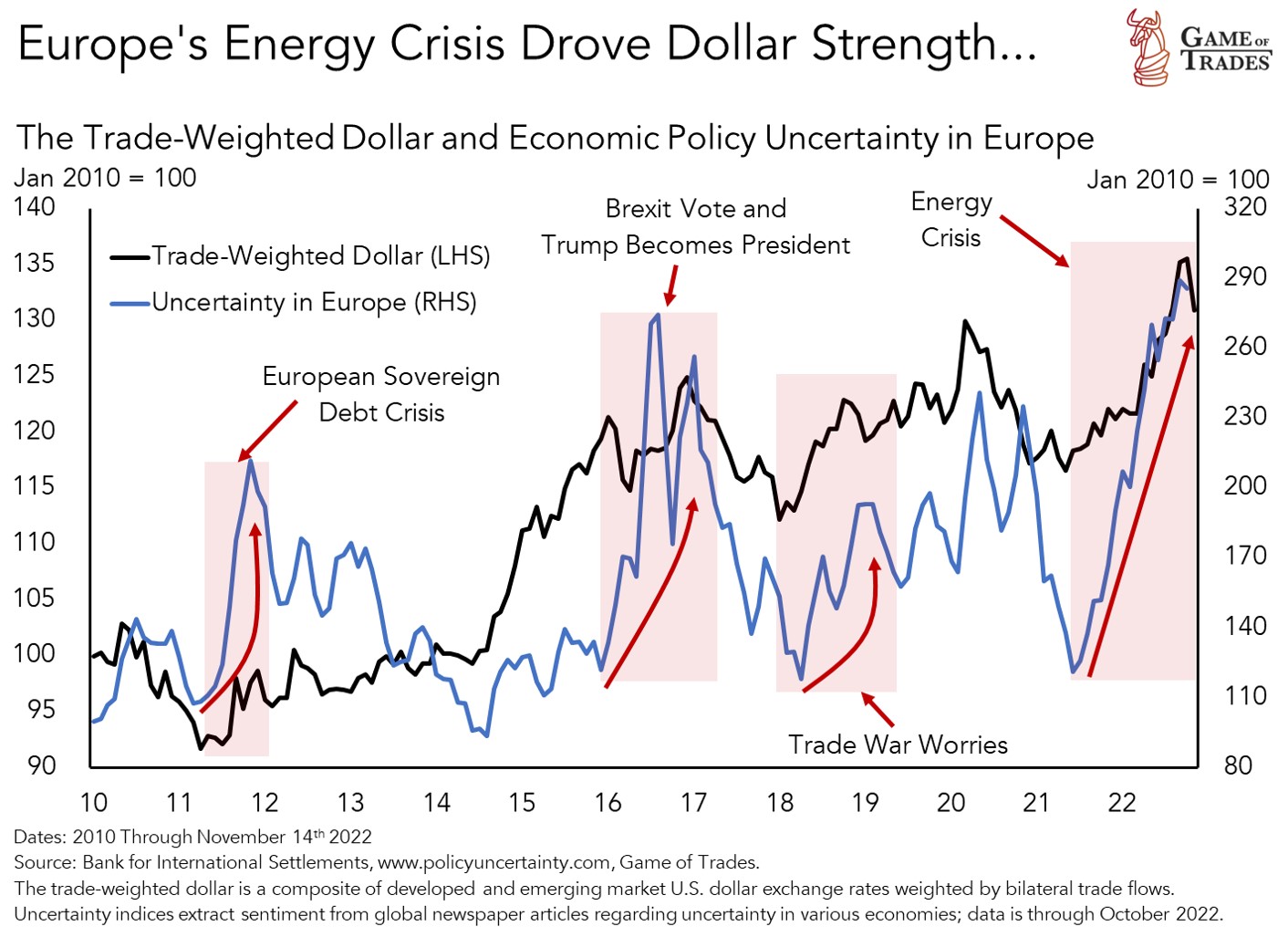

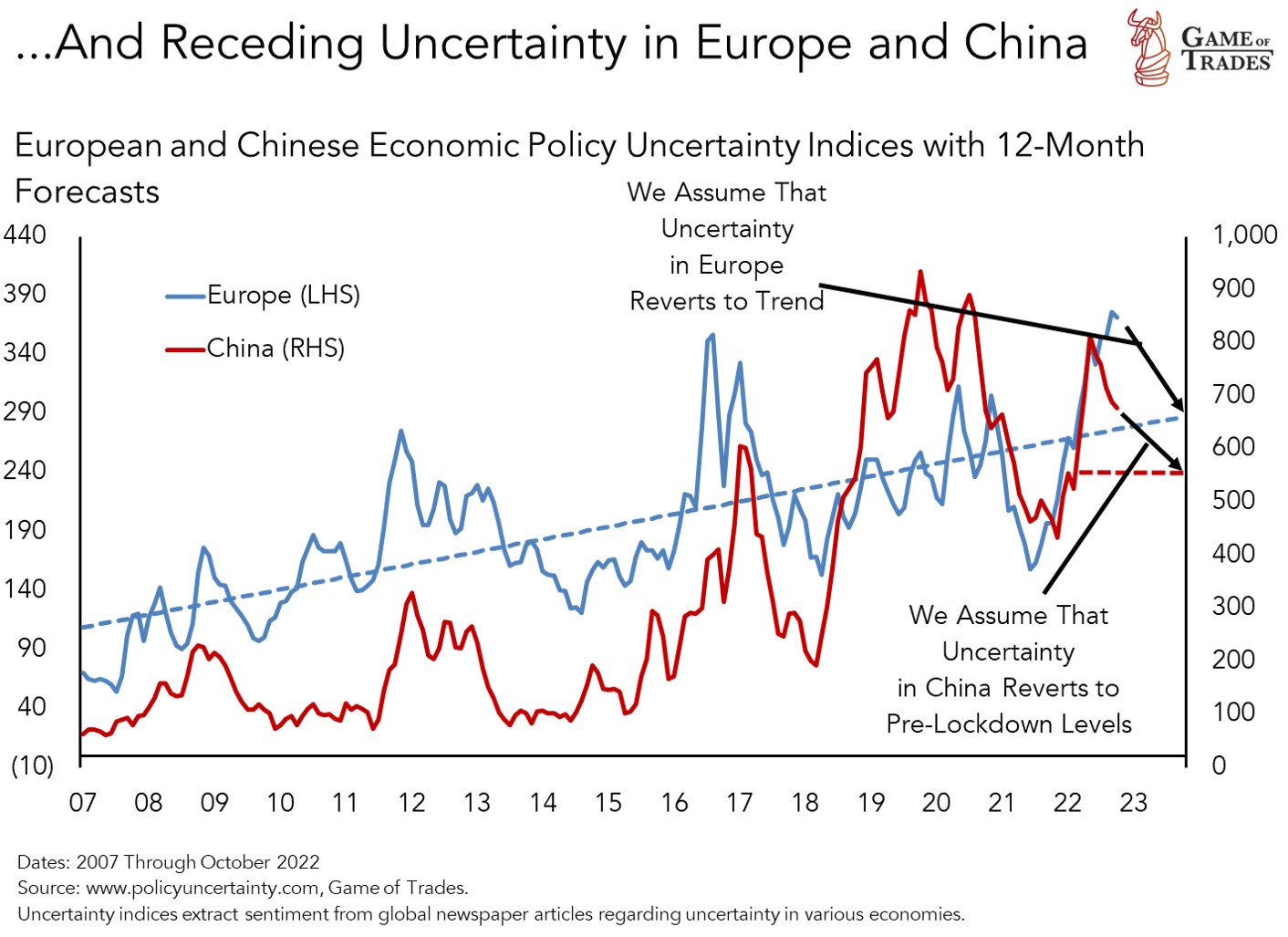

As we documented in our update on the dollar back in mid-August, Europe’s energy crisis has been a driver of dollar strength. The rise in the dollar that began in early-June of last year was driven by rising economic uncertainty in Europe resulting from a supply crunch in natural gas following a post-pandemic boom in demand, as depicted in the chart below.[2] In the post-crisis years, macroeconomic events in Europe like the sovereign debt crisis and the Brexit vote drove dollar strength, as investors sought a safe haven amidst the uncertainty.

China has been another important story driving the dollar’s strength this year. The strict covid-related lockdowns put in place in the spring drove economic uncertainty in China higher, triggering worries of a deep slowdown. The ensuing weakness in the yuan helped drive the dollar higher. Over the last couple of weeks there have been preliminary indications that China is looking to reopen the economy, albeit the pace of it is still uncertain.

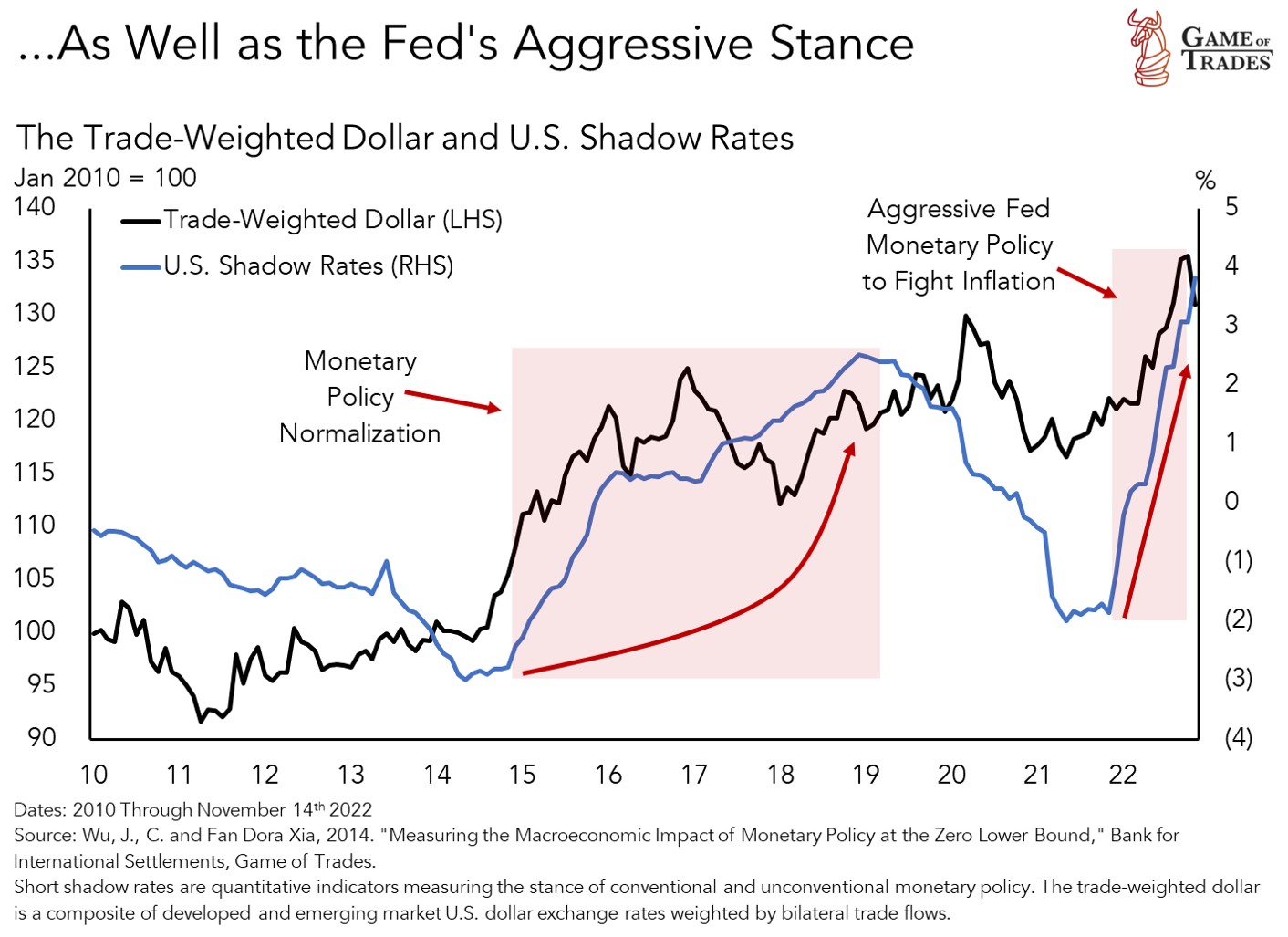

Lastly, the Fed’s aggressive monetary policy stance has also played a large role in driving the dollar higher by widening interest rate differentials between those in the U.S. and the rest of the world. Relatively-higher interest rates in the U.S. are constructive for the dollar, as global investors seek a higher return on their capital and bid up dollar-based assets. As shown in the chart below, rising U.S. shadow rates have been associated with a strengthening of the dollar. As we’ve mentioned in prior research, shadow rates proxy for short-term interest rates by taking into account quantitative easing, capturing how interest rates move when they’re bound by the zero lower bound (i.e., negative rates).

In our quantitative modeling, we found that moves on the dollar are heavily-influenced by changes in interest rate differentials and in economic uncertainty; hence our focus on those two factors.

A Weak U.S. CPI, Falling European Energy Prices and China’s Reopening: A Powerful Confluence Slamming the Dollar

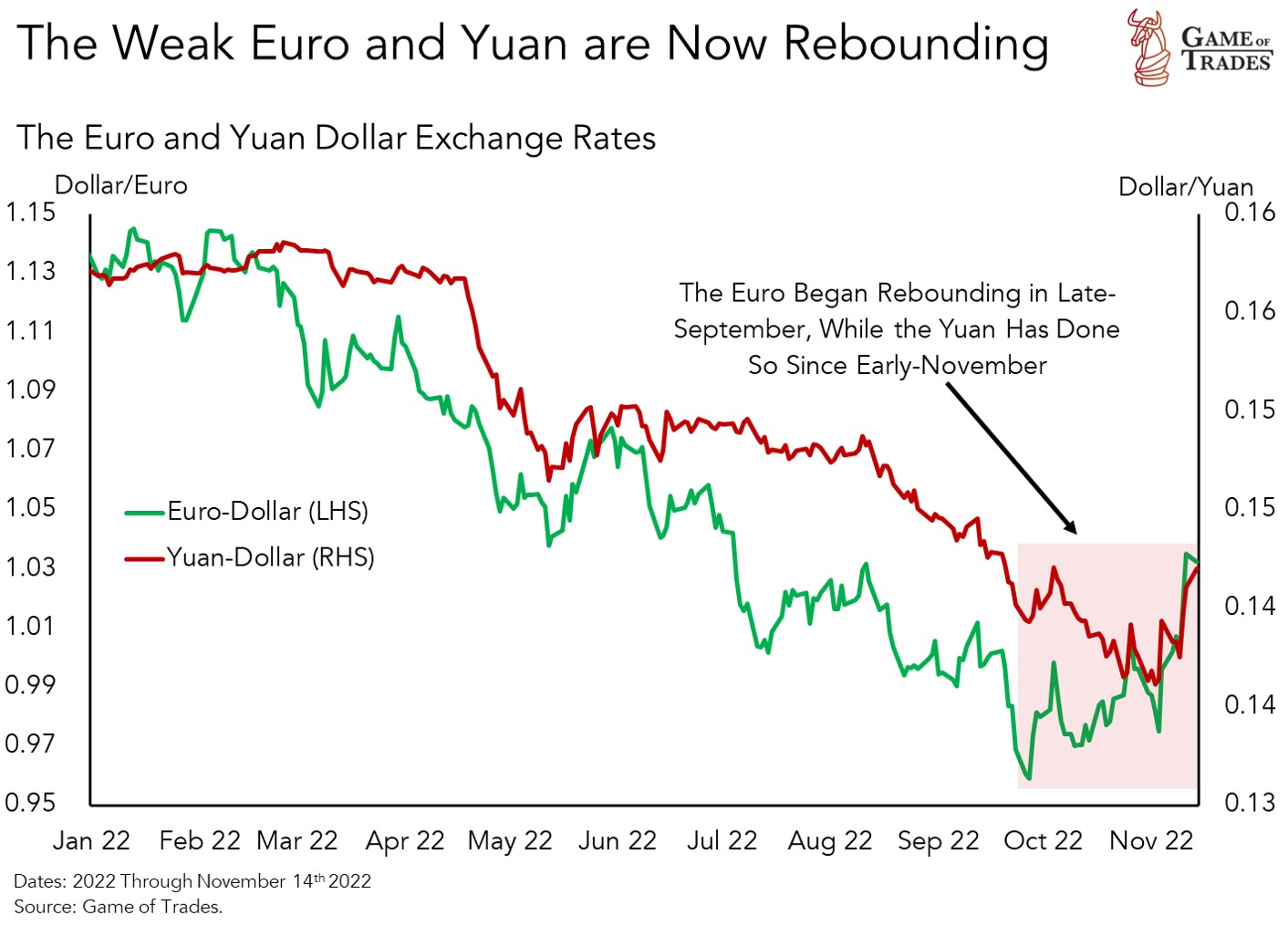

With an understanding of what’s driven the dollar higher in the last year-and-a-half, let’s now focus on what’s driven the weakness of the last few weeks. Since late-September, the euro has seen a big rebound relative to the dollar, as shown below. That’s been the result of constructive developments regarding the energy crisis in Europe, improving the economic outlook. Meanwhile, the yuan has seen big appreciation relative to the dollar since early-November. Recent news that China’s new government will be loosening its strict Covid policies and providing stimulus to its troubled housing market boosted the yuan. We’ll take a closer look at those two developments shortly.

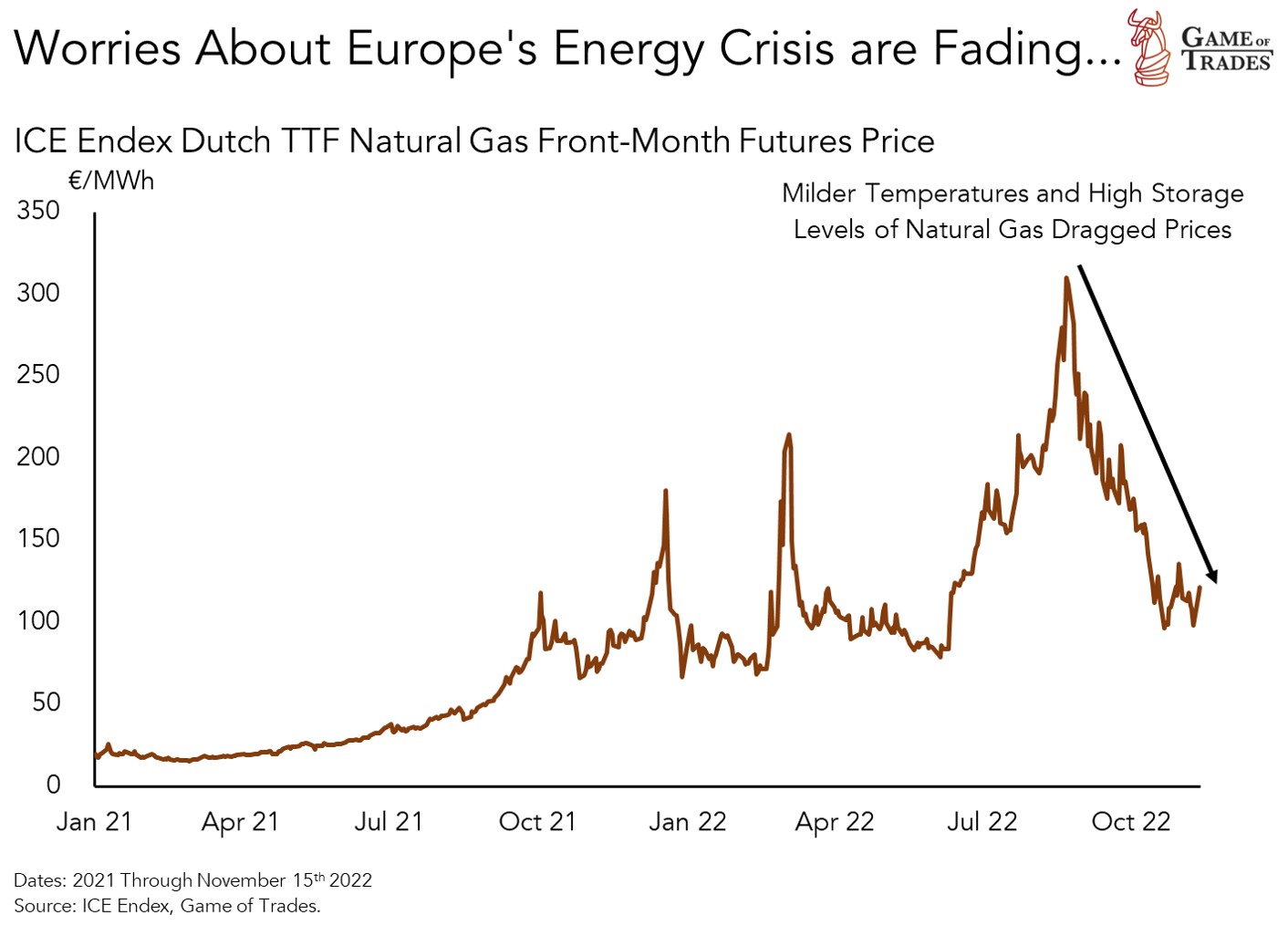

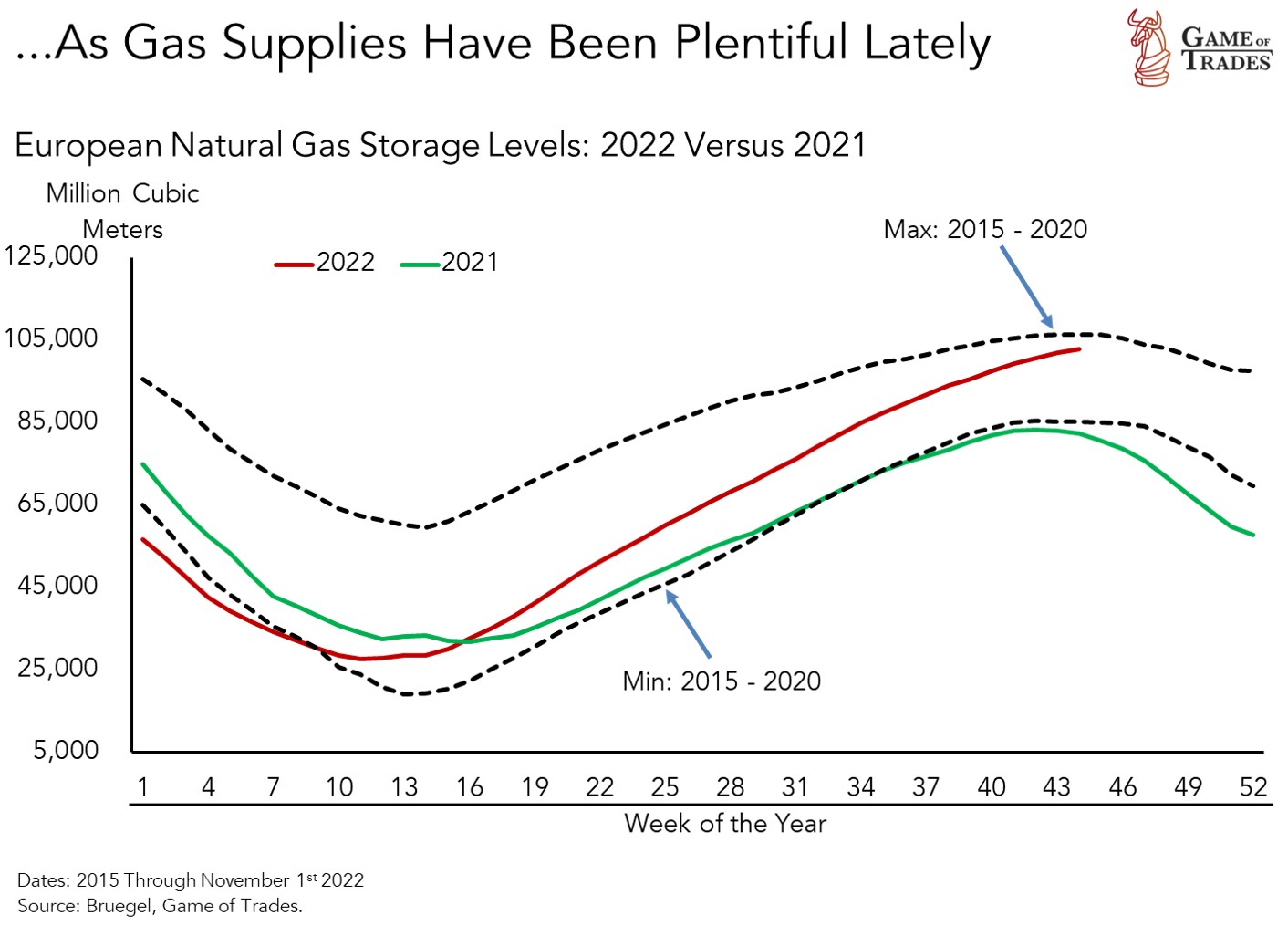

As we documented in our late-October article on Europe, concerns around the energy crisis in Europe have been dissipating. A testament of that is reflected in prices of natural gas in Europe seeing a massive decline following their peak in late-August, as shown below.

One of the drivers has been the surge in natural gas supplies held in European storage. While only a few months ago governments in the region were targeting 80% gas storage capacity, the actual delivered number is about 95% as of today. Europe has proven successful in sourcing gas from all over the world following the crunch that ensued after Russia cut supplies. Another driver for weaker energy prices in Europe has been a winter season that’s featured milder temperatures than expected, reducing demand for the commodity. These constructive developments have rekindled optimism on the euro.

Moving along to the yuan, the currency’s rebound more recently is a story of shifting government policy. In the last couple of weeks, the Chinese government has hinted on loosening their Covid-zero policy, that’s held economic growth hostage since the onset of the pandemic.

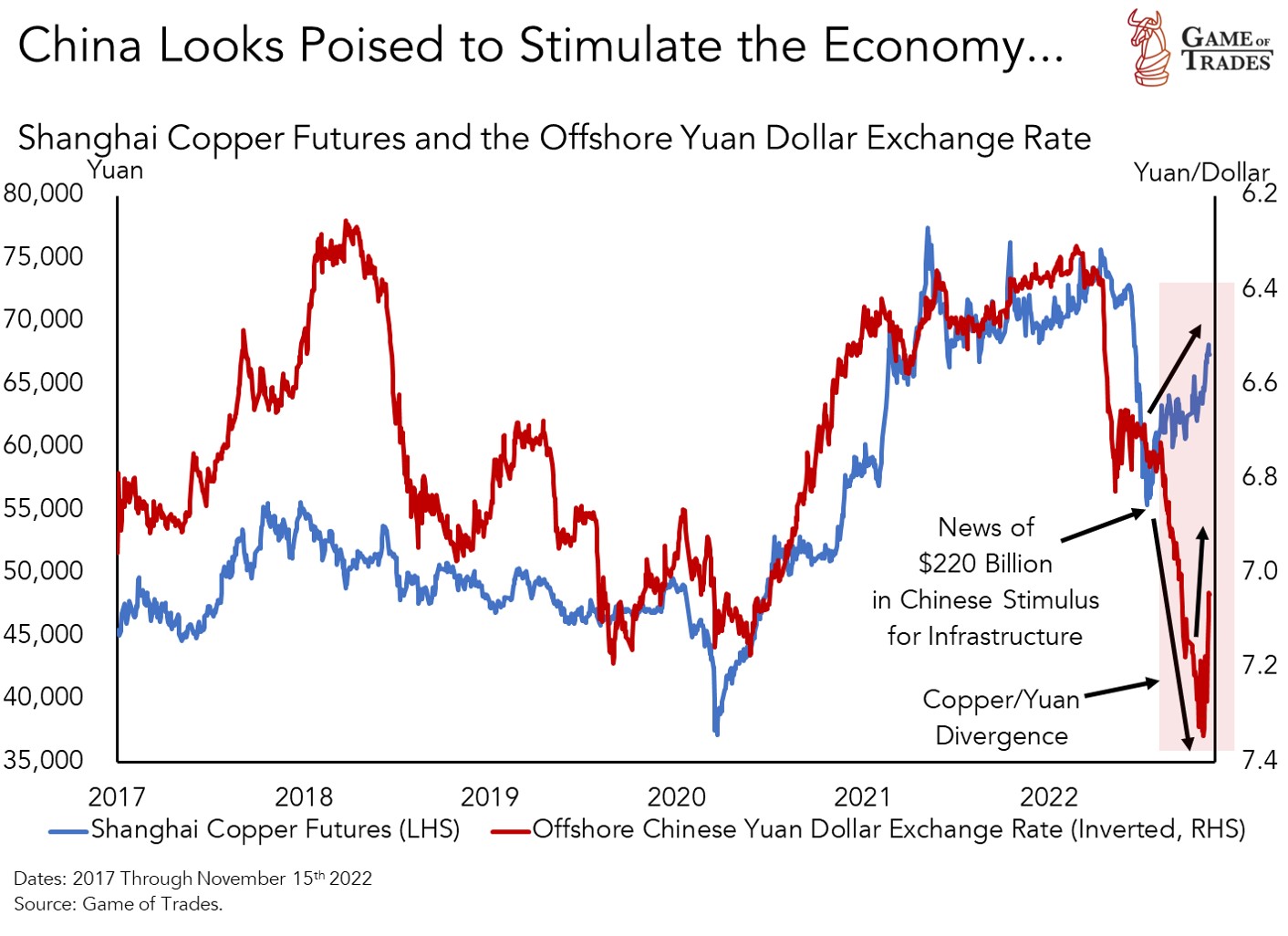

The government has also been guiding at providing stimulus for infrastructure spending. That’s something we brought up in our article on industrial metals from late-August. As shown below, Shanghai copper prices have been moving higher since mid-July following news of a potential $220 billion stimulus package being deployed to support infrastructure spending. Moreover, the government’s 16-point plan on rescuing China’s beaten-down housing sector released over the weekend has also helped catalyze a jump in the yuan. As the chart shows, the yuan looks undervalued relative to copper and is poised to catch up to the industrial metal. Too much pessimism looks priced in the currency.

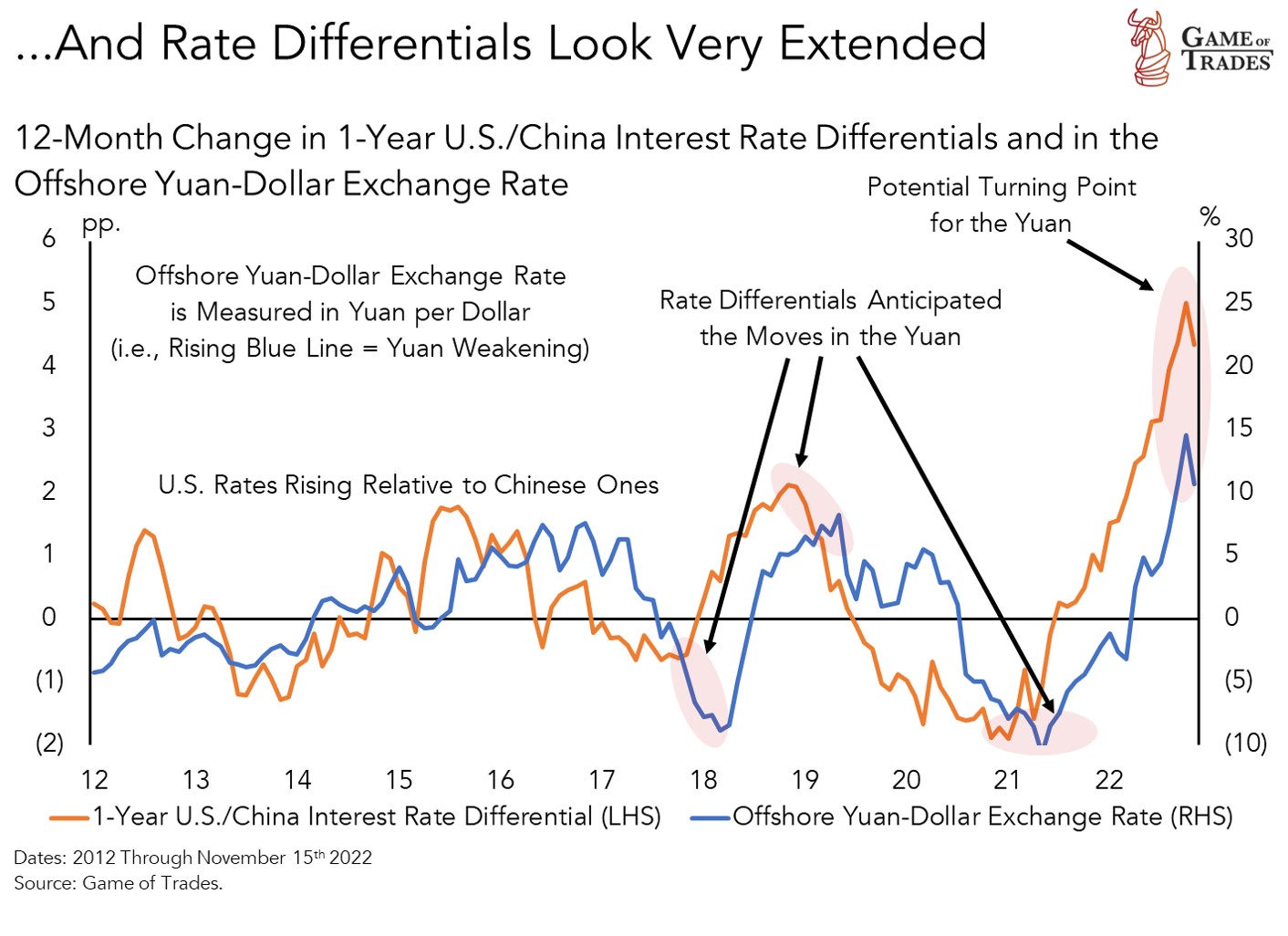

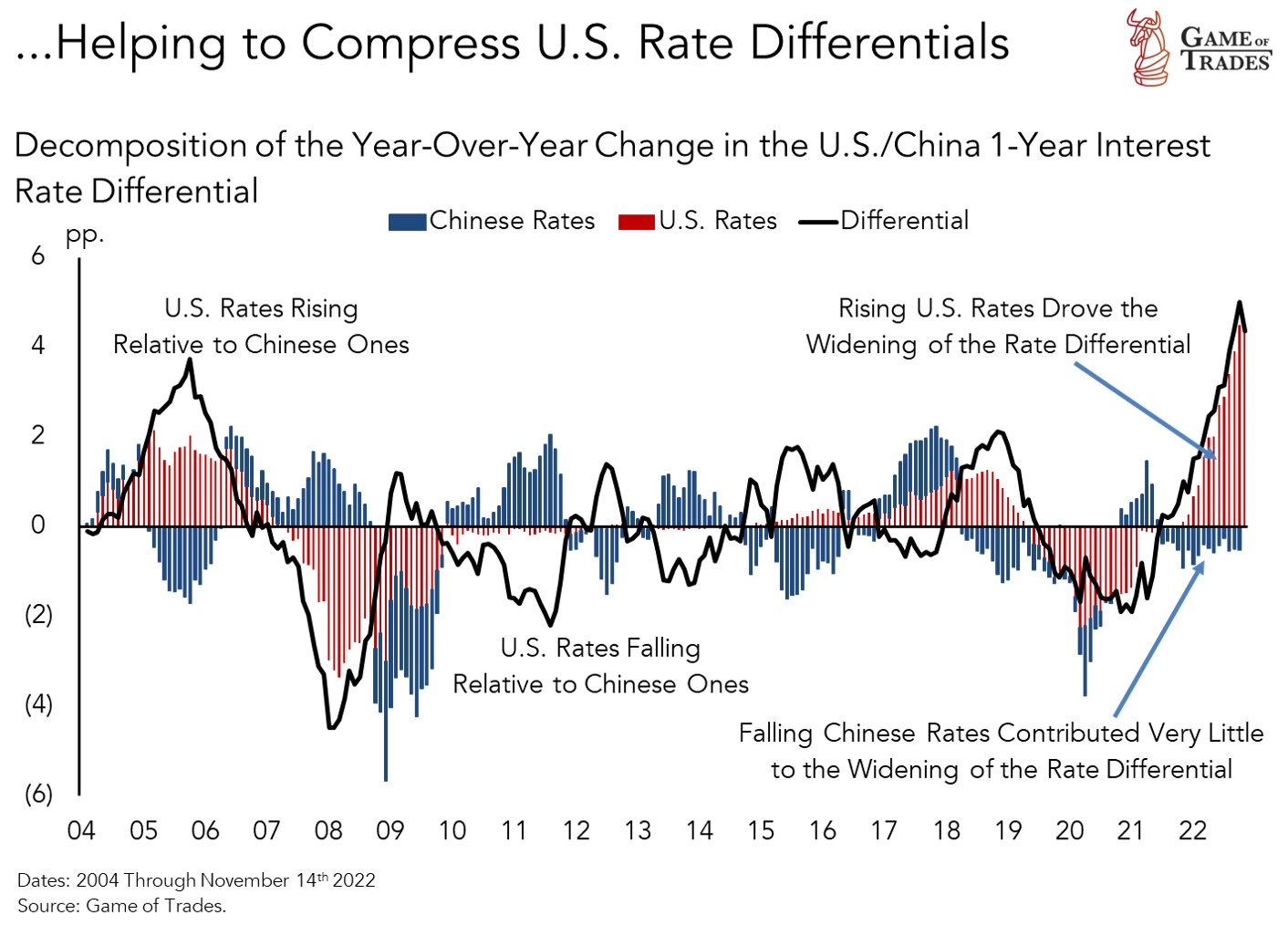

Another driver of recent yuan strength has been the narrowing differential in interest rates between the U.S. and China, as captured by the orange line in the chart below. As the Fed has aggressively hiked interest rates this year to root out inflation, the rate differential widened in favor of U.S. rates. That’s boosted the appeal of holding dollar-yielding assets, with the opposite effect for the yuan. With inflation showing signs of decelerating, and a gradual reopening of China, we expect U.S. rates to head down and Chinese ones to move higher, compressing the differential and boosting the yuan. As evident in the chart, inflection points in the rate differential have anticipated big moves in the yuan in the last few years.

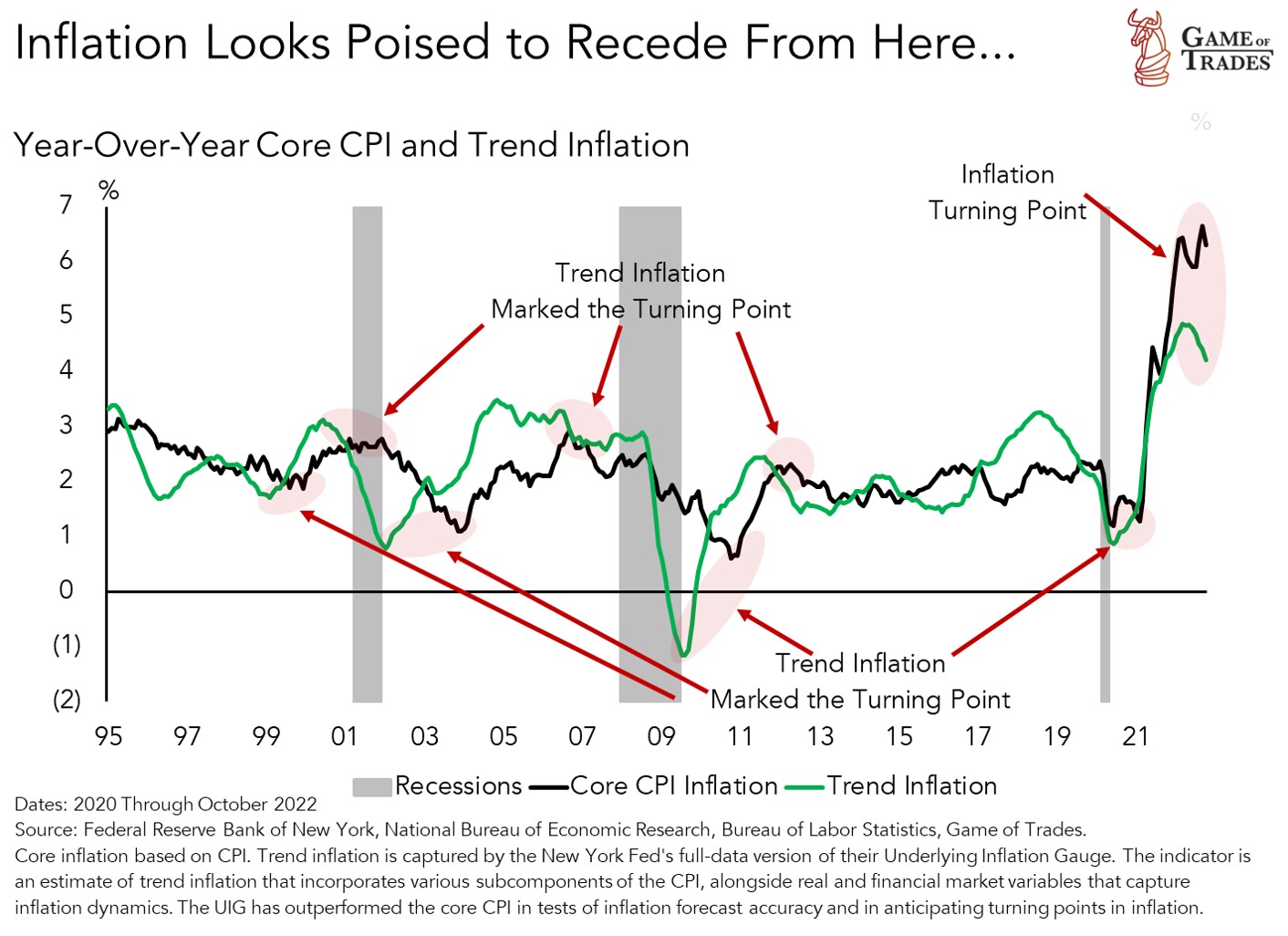

Lastly, the weak CPI print of October has put downside pressure on U.S. interest rates, narrowing rate differentials not only with China but also with Europe. We’ve written extensively in the last few months on inflation dynamics and one of the data points that’s driven our conviction for a deceleration is shown in the chart below. The underlying trend in inflation peaked back in March, and historically it’s proven a good leading indicator of headline and core inflation.[3] We highlighted the usefulness of trend inflation as a leading indicator back in our article from mid-October.

With inflation trending lower, the bias for U.S. interest rates is down. That’s important because widening rate differentials have been a big source of yuan weakness this year. In fact, almost the entirety of the widening this year has been driven by rising U.S. rates, not falling Chinese ones. As inflation inflects downward, the U.S. bond market will start pricing lower interest rates, weakening the appeal for holding dollar-based assets and boosting the yuan. Given the relatively-large weighing of the yuan in the trade-weighted dollar, it’ll become a big source of downside pressure on the greenback.

We Built a Model to Forecast Where the Dollar is Headed

As we mentioned earlier in the article, China and Europe have comprised big stories in driving the dollar in the post-crisis years. As a result, our framework for modeling the dollar today involves an assessment of economic uncertainty in Europe and China, as well as differentials in interest rates between the U.S. and those two economies. To expand on that approach, we built a model for explaining the moves in the dollar based on the below-listed four variables.

- Economic uncertainty in Europe

- Economic uncertainty in China

- U.S/Europe interest rate differentials

- U.S./China interest rate differentials

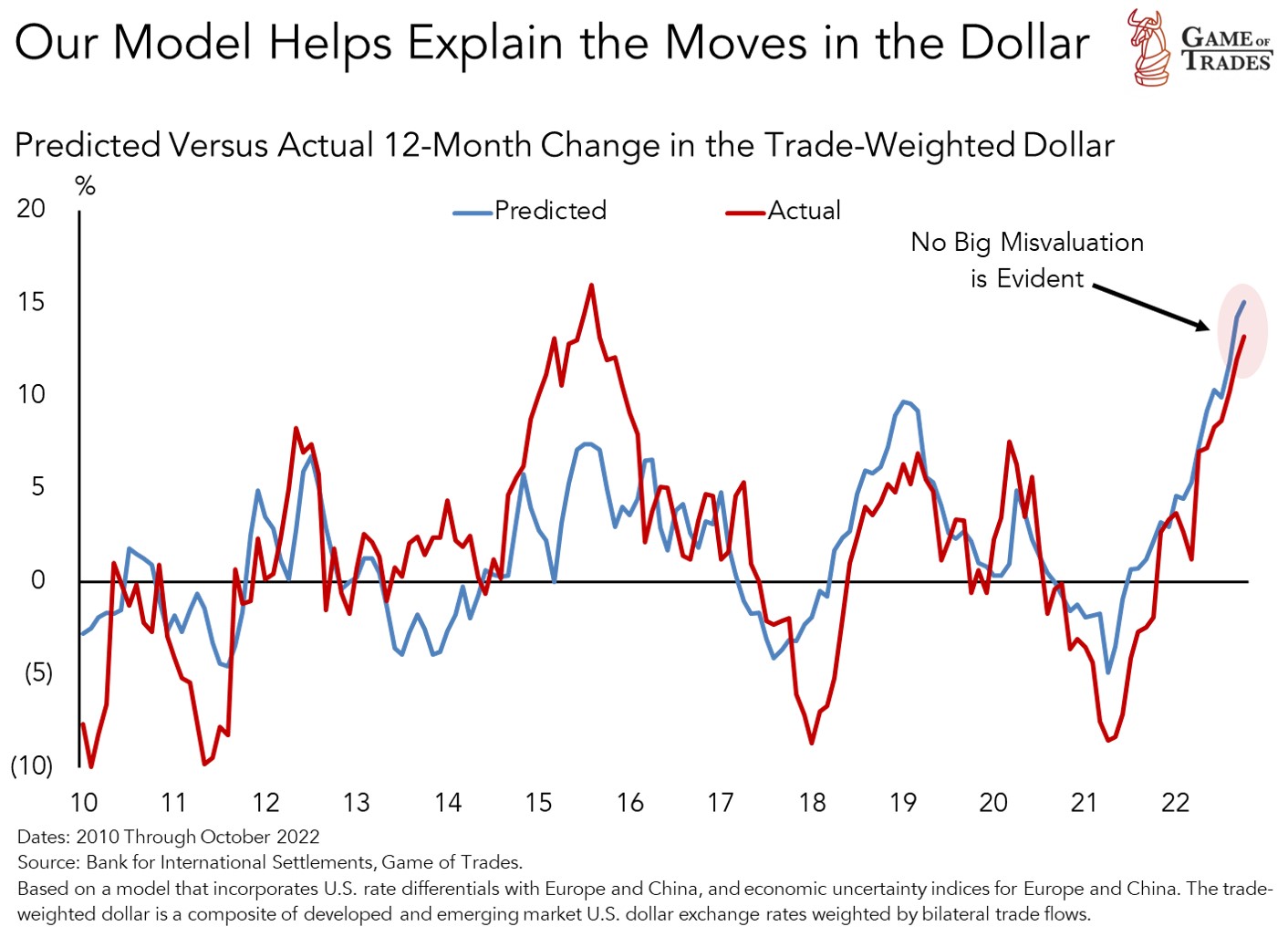

The results of that model are shown in the chart below that depicts the 12-month changes in the dollar alongside the predicted changes based on the four factors we just listed. Those factors have proven accurate in modeling the behavior of the dollar over time, as captured in our model.

To develop a target for the dollar for the next 6-12 months, however, we’d have to make assumptions on how we see rate differentials and uncertainty develop over that horizon. Those inputs will then feed into the model and provide us with a target for the dollar. We take a look at that in the next section.

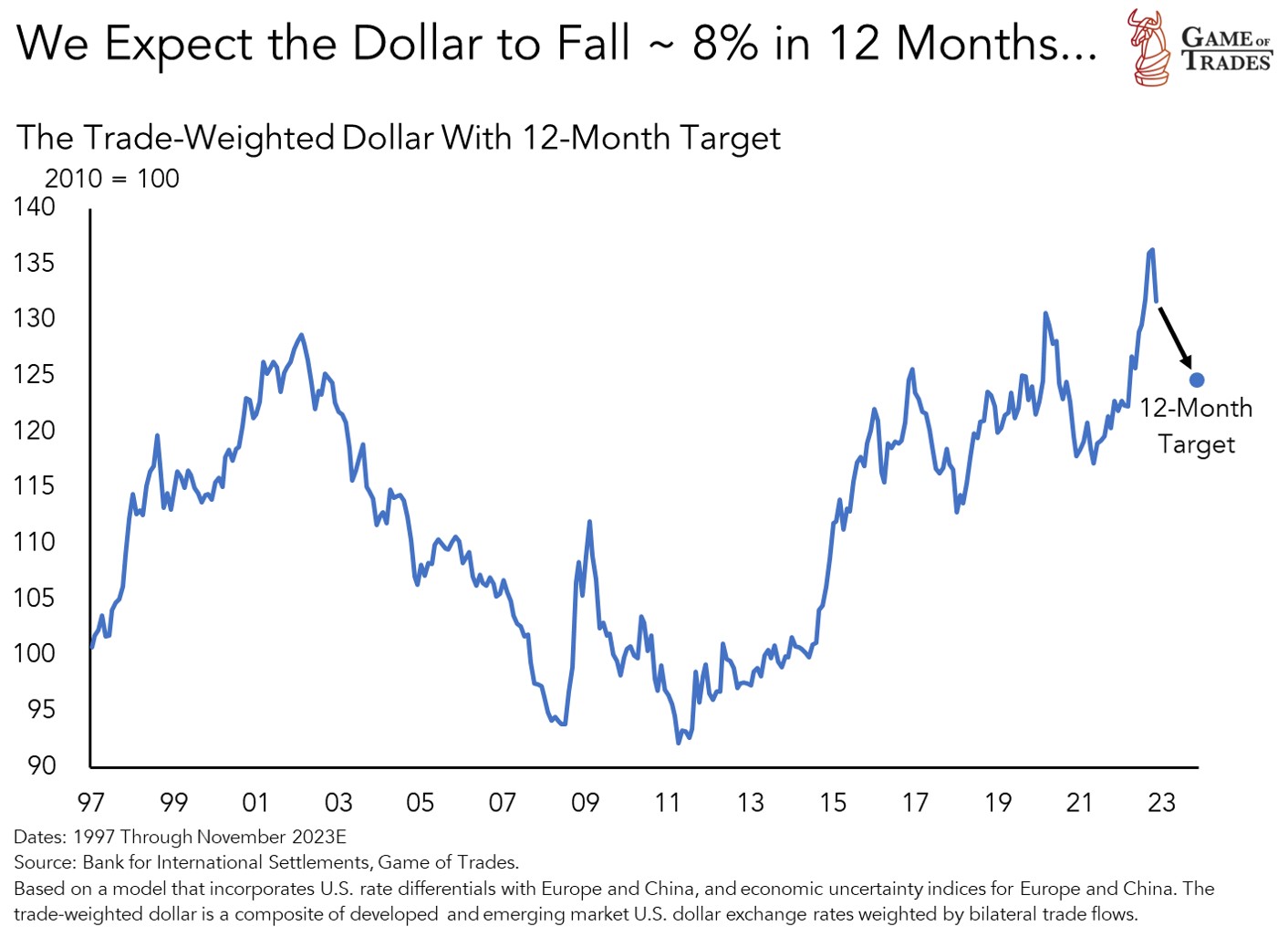

Conclusion: We Expect an 8% Depreciation of the Dollar in the Next 12 Months

We expect a decline in the dollar of about 8% over the next 6-12 months as shown in the chart below. That’s driven by our expectations for positive developments in Europe’s energy crisis, loosening Covid restrictions alongside stimulus policies in China, and receding inflation pressures in the U.S. We’ll now delve into our assumptions in formulating this view.

Our estimates for the dollar are based on the below-listed assumptions regarding how we see interest rate differentials and economic uncertainty develop in the next 6-12 months. As we mentioned those are important variables that feed into our model**.**

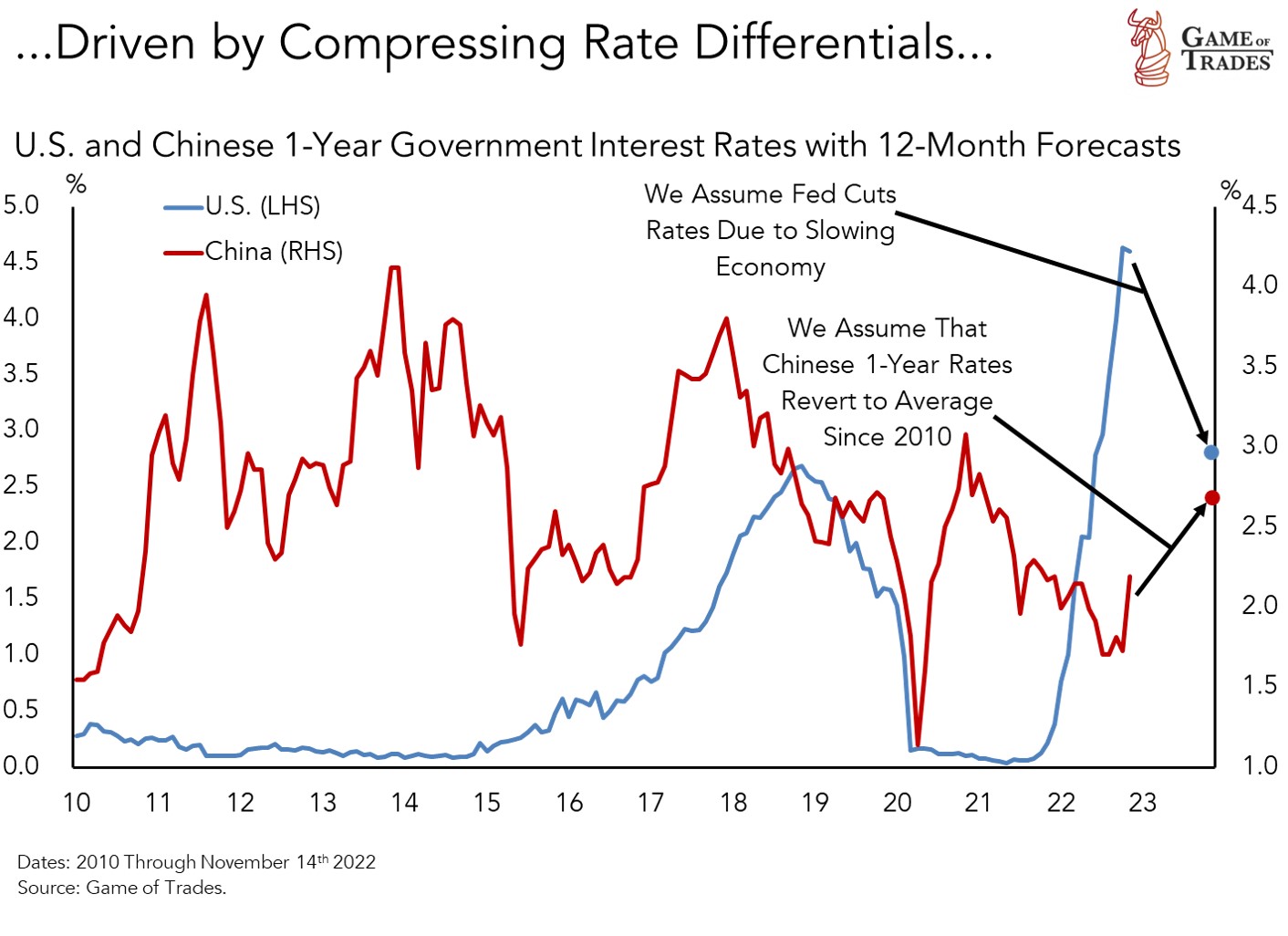

- Receding inflation in the U.S. eases interest rate pressures, driving U.S. rate differentials with respect to China lower. We expect the 1-year government rate in the U.S. to decline to 2.8% as shown below, consistent with our target for the 2-year government yield we highlighted in a prior article. We expect a gradual reopening of China’s economy, bringing higher interest rates in the country as the bond market prices in a higher level of economic activity. We envision 1-year Chinese government rates to rise to 2.7%, matching their average level since 2010 and close to parity with U.S. rates, as shown below.

- In the case of Europe, we assume no change in rate differentials with the U.S. in the next 6-12 months. We expect that the decline in energy prices in Europe, coupled with poor economic growth will gradually reduce inflationary pressures there and limit the runway for the ECB to keep raising interest rates. As a result, we don’t expect a big change in rate differentials between the two economies.

- We assume that worst of the Europe’s energy crisis is over, for now, and that uncertainty will revert to trend as shown by the blue line below. We believe this is a conservative estimate that makes no assumption about Europe’s potential challenges in securing gas for the winter of 2023. We’ll have to assess those probabilities as that outlook becomes more evident.

- Similarly, we expect the policy response in China to drive economic uncertainty down to the level seen earlier this year prior to the lockdowns put in place. It’s our view that the government will have to remove the stranglehold on the economy to mitigate the impact from the afflicted housing market. Our estimate assumes that the authorities’ most recent efforts to contain the real estate slump will help bring about more certainty regarding China’s outlook. If the reopening unleashes pent-up demand from consumers, we’ll likely see an even bigger decline in uncertainty, giving the yuan a bigger-than-expected boost.

Our thesis on the dollar could prove wrong if the reopening in China creates a big spike in Covid cases and fatalities. That may force the authorities to dial back the reopening, bringing another surge in uncertainty. Moreover, hotter than expected CPI readings in the next few months could force the bond market to price in higher U.S. rates, widening differentials.

As we mentioned at the beginning of the article, we’re not making claims on whether the end of the dollar secular bull cycle is at an end. Our call is mainly for a correction of the aggressive move in the dollar that began last year given our view on how the factors that drove it will develop in the next 6-12 months.

In a follow-up article we’ll be bringing to bear our negative view of the dollar to assess what the implications would be for asset allocation more generally, and our model portfolio in particular.

Footnotes:

[1] The trade-weighted dollar is a composite of developed and emerging market U.S. dollar exchange rates weighted by bilateral trade flows. It’s a more encompassing measure of the dollar than the DXY, that only takes into account a handful of developed market currencies like the euro, pound and yen.

[2] Economic policy uncertainty indices extract sentiment from global newspaper articles regarding uncertainty in various economies.

[3] Trend inflation is the underlying inflation rate when removing the noise. It weighs in more than just prices, incorporating real economic activity (i.e., like the ISM prices indices and M2 money supply) and financial market data (i.e., like commodity futures prices) as well. That makes it into a leading indicator on where headline and core inflation is headed.

off topic question: In comparison to M2 money supply, precious metals are pretty cheap now and lumber is historically cheap. Why do you not have gold or other commodities (long) in the model portfolio? I understand the mid term S&P trade based on yields and sentiment, but from an investing standpoint, stocks are not that cheap.

Thanks for the question @Ida Vikman. In our work, gold is a function of real yields (i.e., rising real yields are bad for gold) and the dollar (i.e., rising dollar is bad for gold). Given our negative outlook on the dollar, we’ll be taking a look at whether gold or other precious metals merit a long position in our portfolio.

Based on my understanding of previous articles and videos, GOT has a long-term (between 5-10 years) bullish thesis on precious metals like gold. The GOLD/M2SL ratio was exactly one metric they looked at. However, in the short term (around 6-12 months), because of a war premium on gold this year, they believe gold is overvalued, and TLT represents a better opportunity than gold. Regarding the S&P 500, GOT well acknowledges the long-term downside risk. They looked at the earnings yield, which is close to dot-com bubble levels. However, they believe that declining inflation and the lag time between rate hikes and an earnings recession provide a window of opportunity for a short-term (6-12 months) bet on the S&P 500. (PLEASE CORRECT ME IF I HAVE SUMMARISED ANYTHING WRONG.)

That’s a great summary @Samonita Kayden. Thank you for sharing that! Yes, we believe gold to be overvalued at the moment as it’s trading at higher prices than warranted by the rise in real yields. Of course, gold could be proven right if real yields do see a big decline here. A falling dollar, however, may boost the value of gold. That’s because gold’s overvaluation is mainly a function of real yields, not the dollar. The dollar falling from here would be “new” information for the gold price, and hence could see appreciation. That’d be particularly true if the dollar falls alongside receding real yields.

Thank you guys for clarifying. I think sometimes when there is a lot of detailed information it can be hard to remember or understand the conclusion.

Given 1) the huge divergence between copper and the Yuan (mentioned in the article), which could be indicating a significant appreciation of the Yuan ahead, 2) the expectations by GOT that the rate differentials between China and the US would narrow, while that between Europe and the US would remain unchanged, and 3) historic low valuations for Chinese stocks, does GOT think Chinese stocks will beat their European counterparts (for the next six to twelve months)?

@Samonita Kayden That’s a great question! That’s something we’re looking to address through an article next week. We’ll be looking at the implications of a falling dollar on equities (U.S. versus non-U.S.), as well as commodities like oil, precious and base metals. Since the peak in the trade-weighted dollar of October 21st, MSCI China has underperformed the MSCI Euro Area in both U.S. dollar and local currency basis.

Here is the question that I have about China. Covid was the most contagious virus in a 100 years. How can a country the size of China avoid this virus completely? The lockdowns would have to continue for a year or two longer. If lockdowns stop then what happens to the unvaccinated population and work production (like the Apple factory that is missing 100,000 workers after a breakout). What happens to China’s controlled currency when in financial distress? They are flooding money in to infrastructure and opening rules on real estate. Will this work if there is a trust issue in banks and the real estate sector? I just don’t see how this ends well for China. Maybe if the current version of Covid is not too dangerous they just open up and lose a minimum of people but their stance and media cause people to get scared. This is a difficult pivot.