Here’s the video version of the article:

Summary

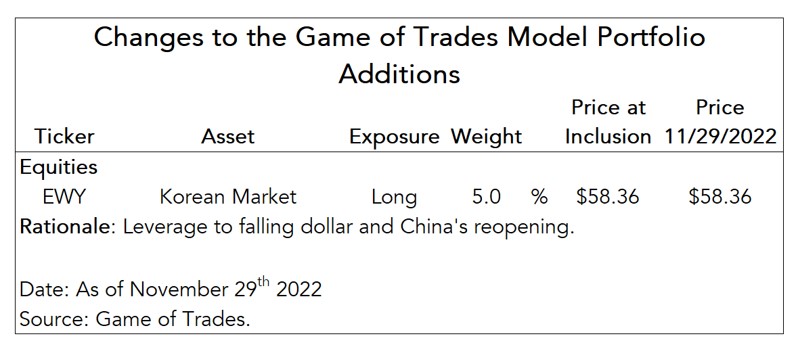

- Expanding on our thesis of dollar weakening, we’re adding Korean stocks (EWY) to our model portfolio. We see them as optimal bets on further weakness in the greenback and China’s reopening.

- Since the early-1970s, the dozen episodes that witnessed a falling dollar saw emerging market stocks outperform their global peers. Within that group, Korean equities generated the best track record.

- Korean stocks are levered to China’s credit impulse, a measure of how fast credit is growing in the country. As China stimulate its economy, a reopening should make Korean stocks big beneficiaries.

- Korean equities are valued attractively, with earnings yields above those seen across most regions. Moreover, the Korean won looks poised to appreciate, boosting returns for U.S.-based investors.

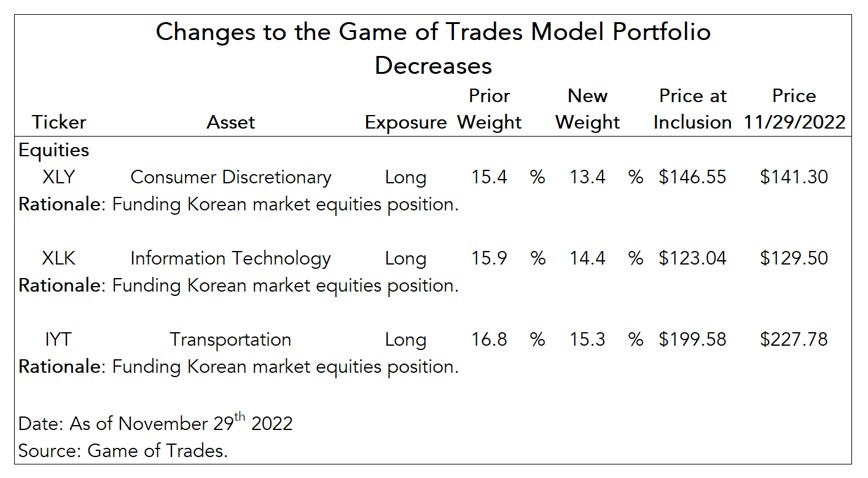

- We’re opening a 5% allocation to Korean stocks via the EWY ETF. That’s funded by trimming our U.S. equity positions in XLY, XLK and IYT. Our U.S./non-U.S. equities split is now about 70/30.

Expanding Our Dollar-Weakening Thesis to Non-U.S. Stocks

In an article posted earlier this month, we provided our thesis on why we expect the dollar’s recent weakness to continue over the next 6-12 months. To capitalize on a weakening dollar, last week we added exposure in our model portfolio to copper miners (COPX) and silver (SLV). Both asset classes have historically shown strength in episodes of dollar weakening given their high sensitivity to the greenback’s moves (i.e., high beta). Moreover, the copper miners are trading at very attractive free cash flow yields, indicating there’s a lot of skepticism regarding the sustainability of their free cash flow production. We’re betting against that skepticism.

Given the dollar’s importance in the global economy, its moves can be very influential for the returns of U.S.-based investors holding foreign stocks, like emerging market ones, for example.[1] Given our view that the dollar is poised to depreciate over the next 6-12 months, increasing our exposure to foreign equities would provide an advantage in outperforming the S&P 500. We’ll discuss that in more detail later in the article.

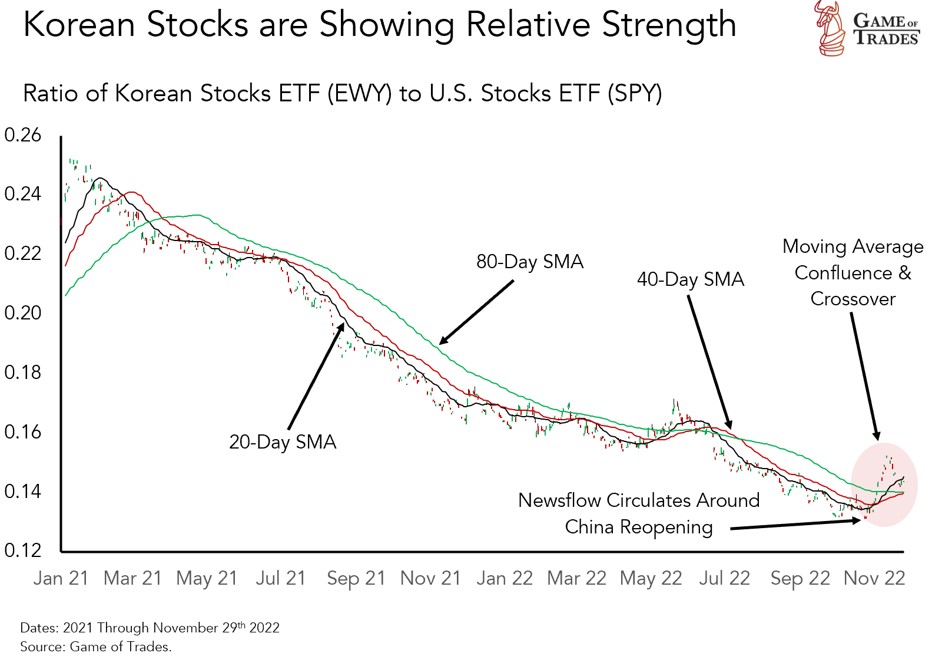

In this research we present our case for adding South Korean stocks to our portfolio. We found the group to be the best expression across global equity markets to capitalize on upcoming dollar weakness, with China’s reopening an important theme. Relative to the S&P 500, Korean stocks have been outperforming since November, when headlines around China potentially relaxing their strict Covid containment policy came to the fore, as shown below.

Emerging Market Stocks: Winners When the Dollar Weakens

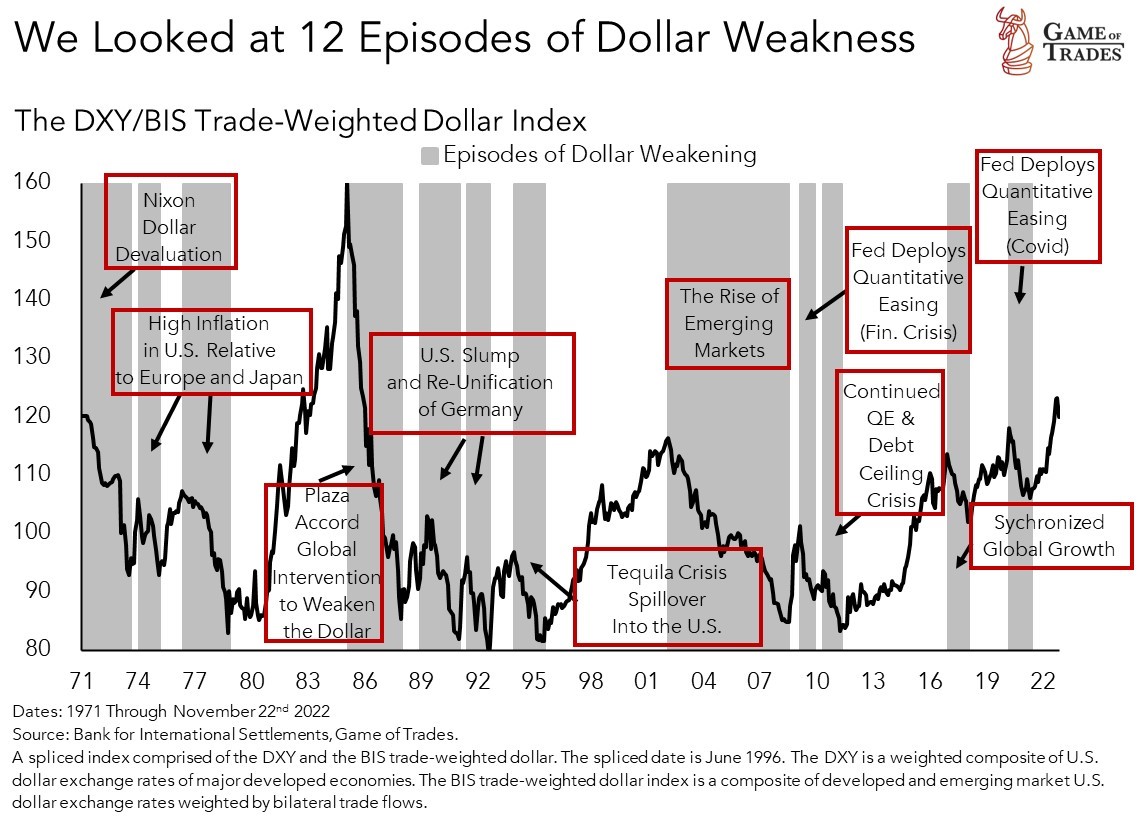

We’ll start by evaluating the performance of U.S. and non-U.S. stocks across a dozen episodes of dollar weakness that we identified going back to the early-1970s. We used a similar approach in our analysis of metals and miners last week, looking for evidence of where the odds look more favorable. The chart below captures the episodes of dollar weakness in gray.

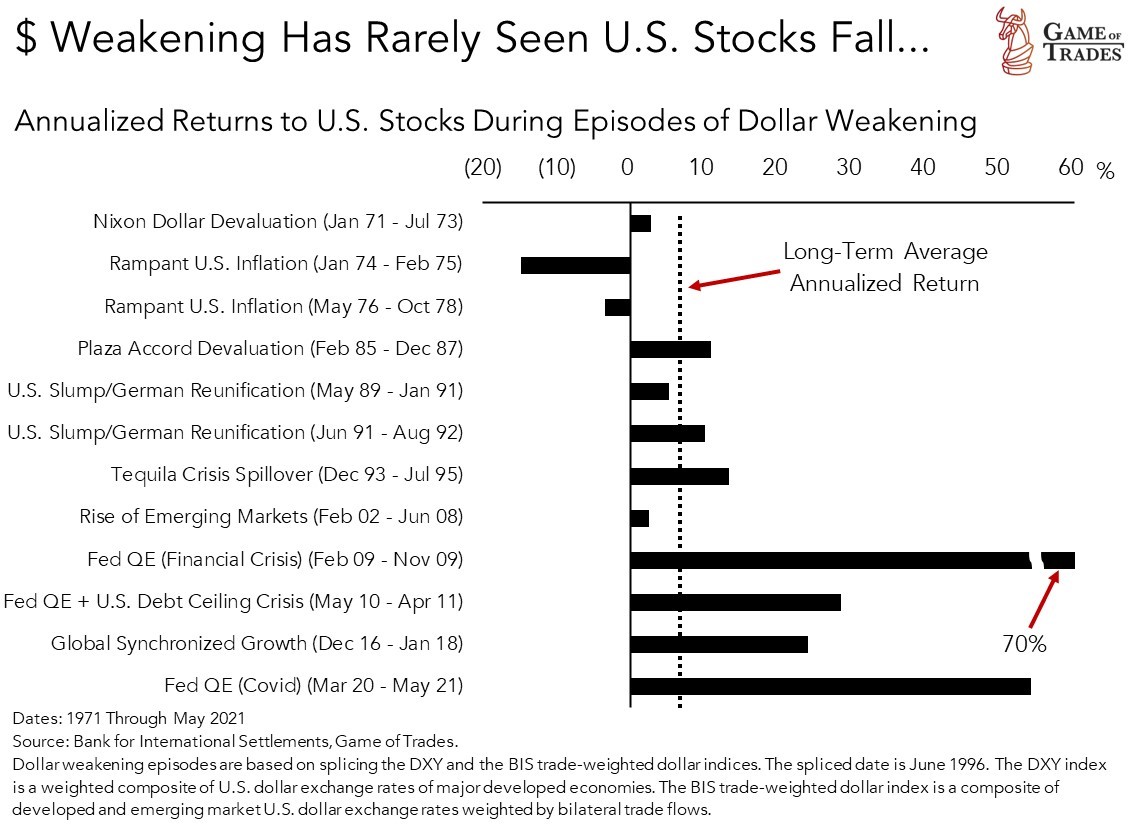

Of note, a constructive statistic: episodes of dollar weakness rarely saw U.S. stocks fall. In fact, returns across the episodes were generally higher than what we’d expect based on the historical average, captured by the vertical dotted line. That was particularly true in the post-crisis years when a weaker dollar became a big tailwind for risk, signaling liquidity injections from the Fed in a backdrop of weak global growth.

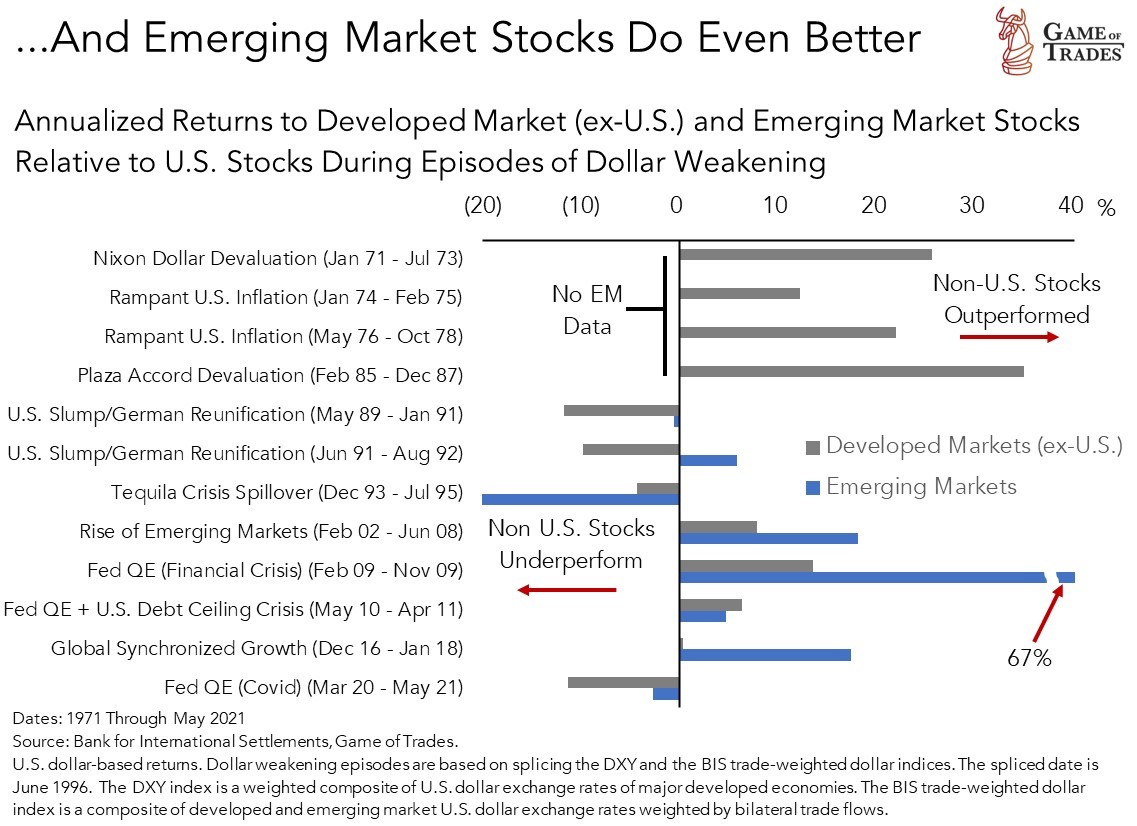

The chart below repeats the analysis from the prior chart, but for the relative returns of non-U.S. stocks (i.e., relative to U.S. stocks), separating between developed and emerging market stocks. As we can see from the chart, there are a lot more bars populating the right side of it. That means that non-U.S. stocks generally outperformed their U.S. counterparts when the dollar weakened.

Across the episodes, on average, emerging market stocks generated 26% per year in the episodes since 1989, when their return data became available. By comparison, U.S. and non-U.S. developed world stocks generated 15% and 16%, respectively. So the odds do favor emerging market stocks.

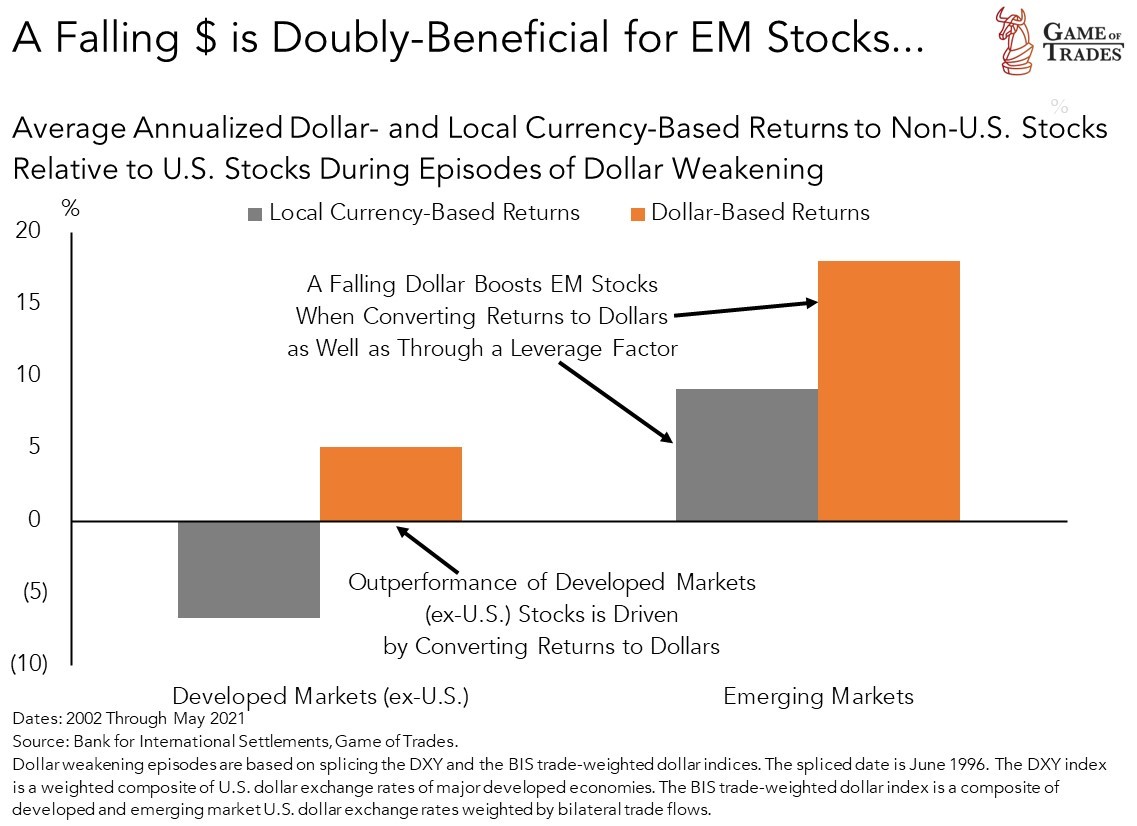

We believe the outperformance of emerging market stocks during periods of dollar weakness has to do with a leverage effect that’s not prevalent in the returns of non-U.S. stocks drawn from the developed world. We can see that in the chart below that depicts the relative returns (i.e., relative to U.S. stocks) to both groups in both a local currency and dollar basis in the globalization decades.[2]

Unlike the case for non-U.S. developed world stocks, the local currency returns of emerging market equities were positive. Dollar-based returns were about twice as strong as we’re explicitly looking at episodes when the dollar was falling. The positive returns in local currency (i.e., excluding the mechanical impact from converting returns in local currency to dollars) are indicative that there’s more to the outperformance of emerging market stocks than just the conversion effect. That leverage effect could be related to the falling dollar stimulating growth worldwide through a loosening of financial conditions. Emerging markets are the primary beneficiaries of stronger global growth given their big role in global manufacturing supply chains and as commodity exporters.

On the other hand, for non-U.S. stocks drawn from the developed world, the outperformance is mainly a mechanical function of converting the returns from local currency to dollars. In fact, on a local currency basis, those stocks generally underperformed U.S. equities during episodes when the dollar fell.

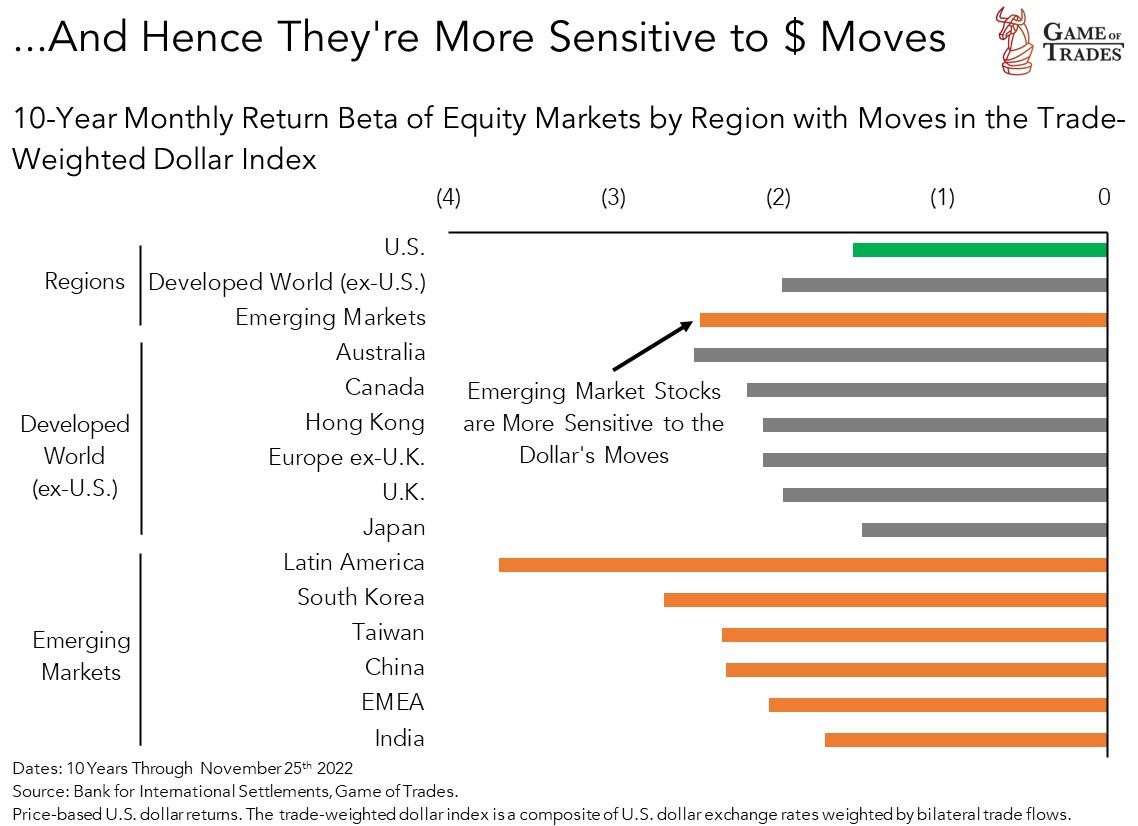

We can compare the leverage effect from a falling dollar across various equity markets globally in the next chart. It depicts the betas of global equity markets to moves in the dollar in the last decade. The beta of emerging market stocks to the dollar was about 50% higher than that of U.S. stocks, and 25% higher than that of those in the non-U.S. developed world. Within the emerging markets group, Korean stocks had the second-highest beta after Latin American stocks. Of course, beta is a backward-looking variable and we can’t just assume that if the dollar were to fall we should blindly bet on Latin American stocks. The quantitative insight from the betas is only part of the analysis, not the whole of it.

Korean Stocks: Best of the Best, Today

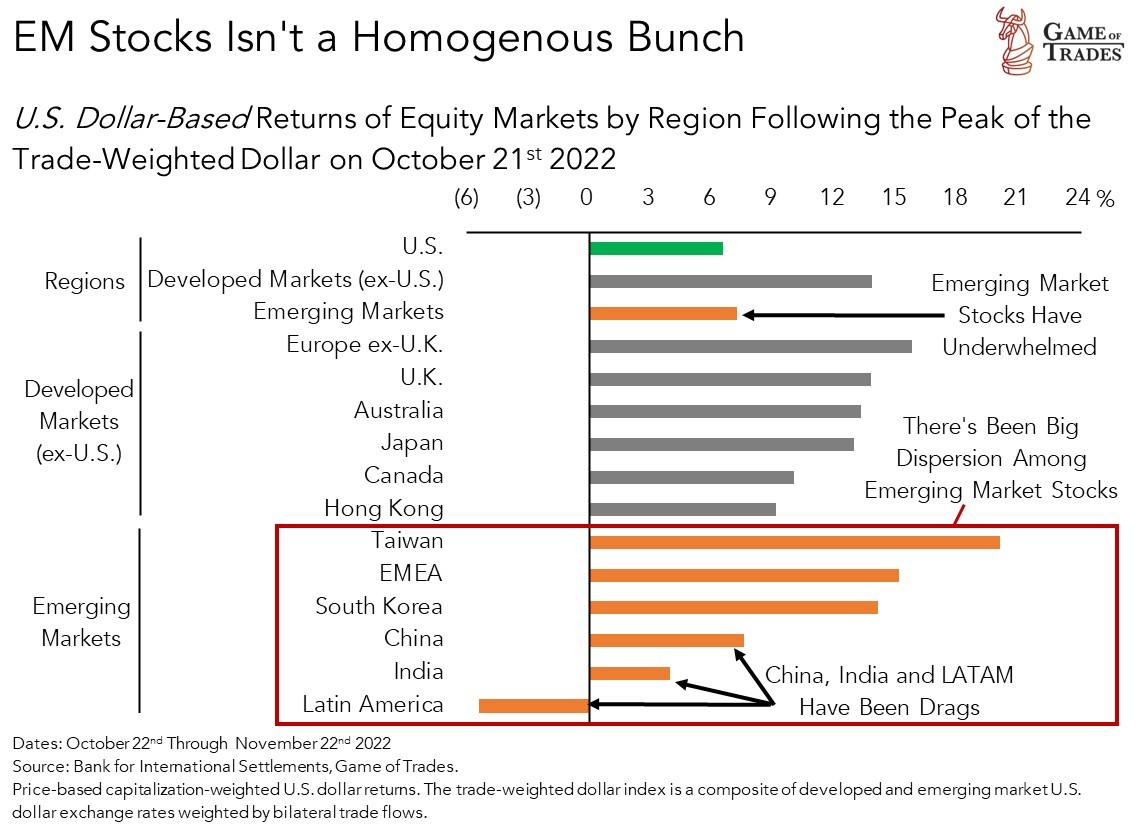

With the historical insight under our belt, we zoom in to today. Korean stocks have outperformed most regions since the recent peak in the dollar of late-October as shown below. They’ve trailed only Europe (ex-U.K.), Taiwan and EMEA. China and India have been a drag for the emerging markets group, as together they make up more than 40% of its market capitalization.

Latin American stocks, that historically showed the most negative beta to dollar moves, have seen big underperformance; a testament that beta isn’t everything. One issue is that some of the major LATAM currencies like the Mexican peso and the Brazilian real appreciated relative to the dollar in the latter’s period of strength. Their exposure to rising commodity prices and aggressive monetary policy played a role in drawing interest to those currencies. However, that meant less upside to the stocks from LATAM currency appreciation.

Of note, there’s been big dispersion seen among the returns to emerging market stocks lately, as captured by the chart above. That highlights an important disclaimer: emerging markets isn’t a homogeneous block. Making a blanket bet on emerging market stocks simply because the dollar is expected to fall isn’t an optimal expression of dollar downside in equity markets. In the next section we go over our framework in choosing Korean stocks as an opportunity to capitalize on the falling dollar.

Looking for Currency + Valuation Tailwinds

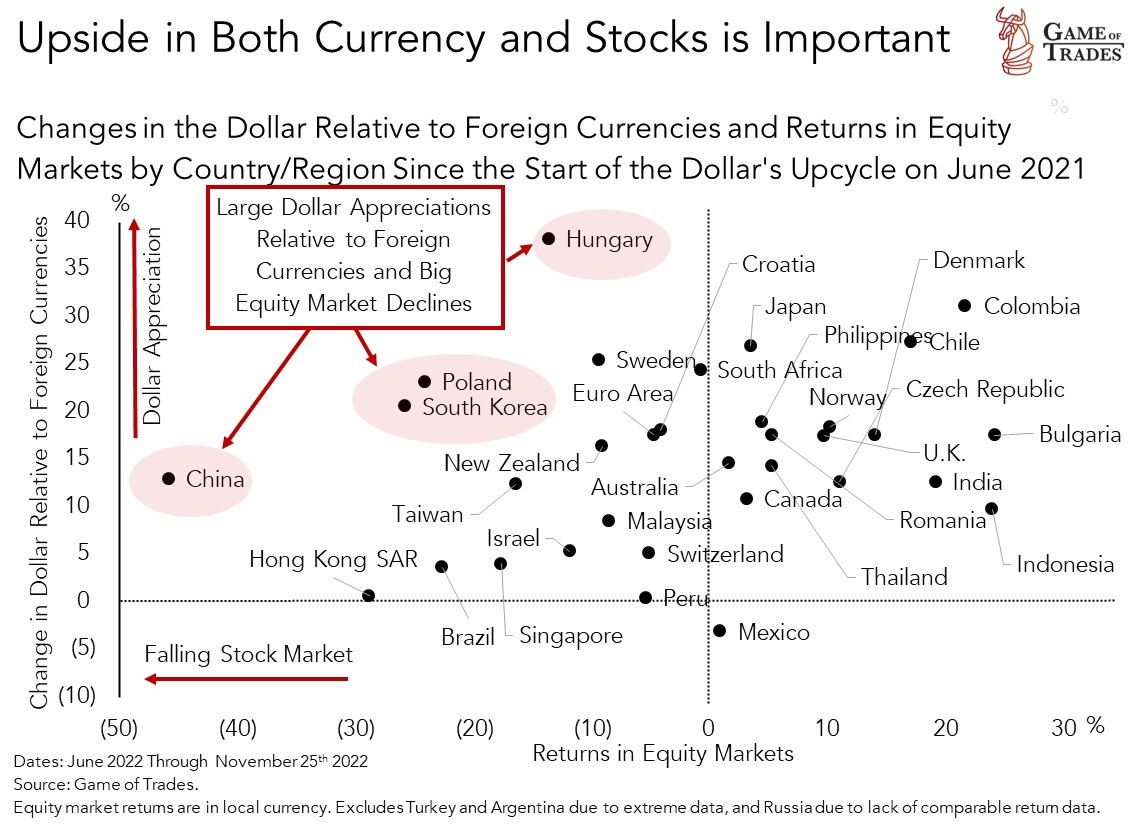

When choosing stocks to favor in the current episode of dollar weakness, we deployed a framework that weighs in upside to both the foreign currency and the corresponding equity market. That framework is shown in the chart below that plots the change in the dollar relative to foreign currencies throughout the greenback’s upcycle that began in June of last year (higher values = bigger dollar appreciation relative to the foreign currency), as well as the corresponding equity market returns (values to the left = bigger equity market drawdown). Based on this approach, Korea, China, Poland and Hungary stand out among the crowd. That helps us narrow the opportunity set.

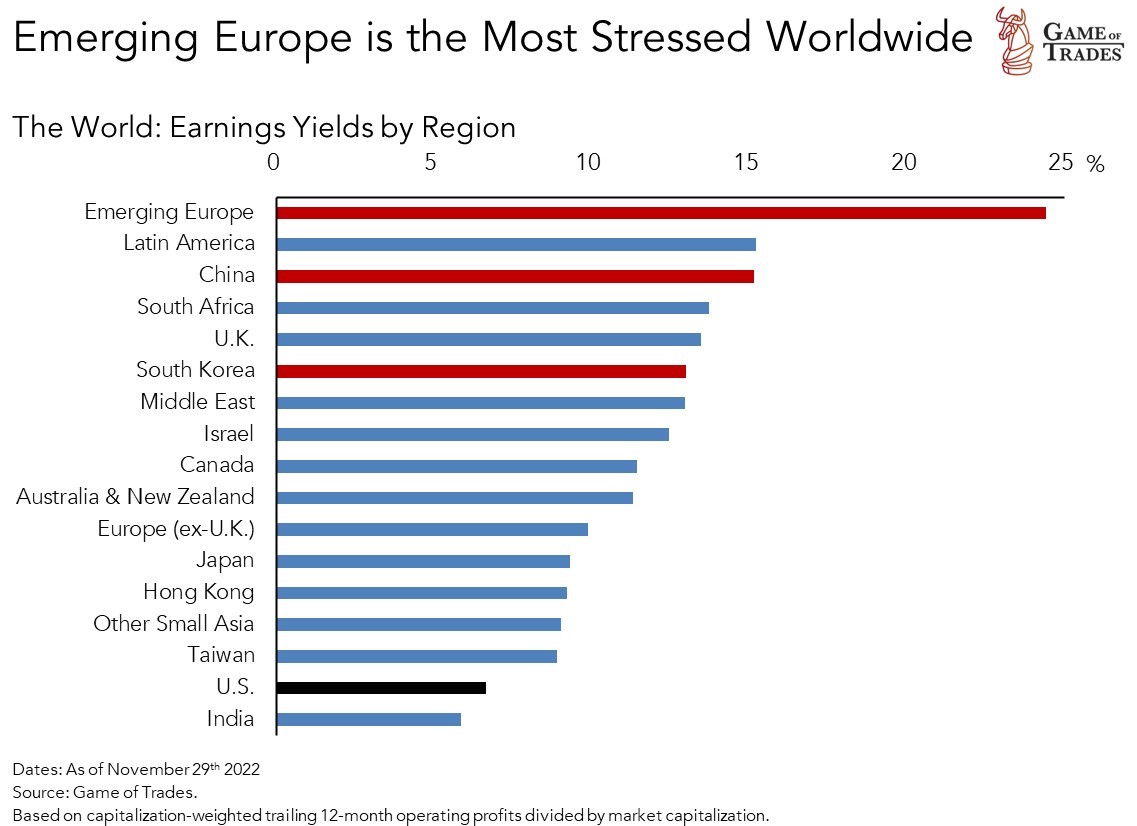

The next step is assessing where valuations look more attractive. The idea is that we want to bet on countries where a significant amount of bad news is already priced into the stocks. That increases the asymmetry of the opportunity, maximizing the upside while minimizing the downside. The chart below provides a point-in-time assessment of the earnings yields by region (i.e., the inverse of the P/E ratio).[3] Emerging European equities, that include Polish and Hungarian stocks, are a clear standout here. We’ll take a look at them next.

Emerging European Stocks are Extremely Cheap, and Risky

The uncertainty surrounding Europe’s energy crisis is the highest seen in close to 30 years. As we’ve documented in our update on Europe from late-October, European governments have proven adept at sourcing natural gas for the 2022 winter season, bringing prices of natural gas down from extreme levels. In early-November we added German small-caps to our model portfolio to capitalize on what we believe is an excessive amount of pessimism priced into the stocks.

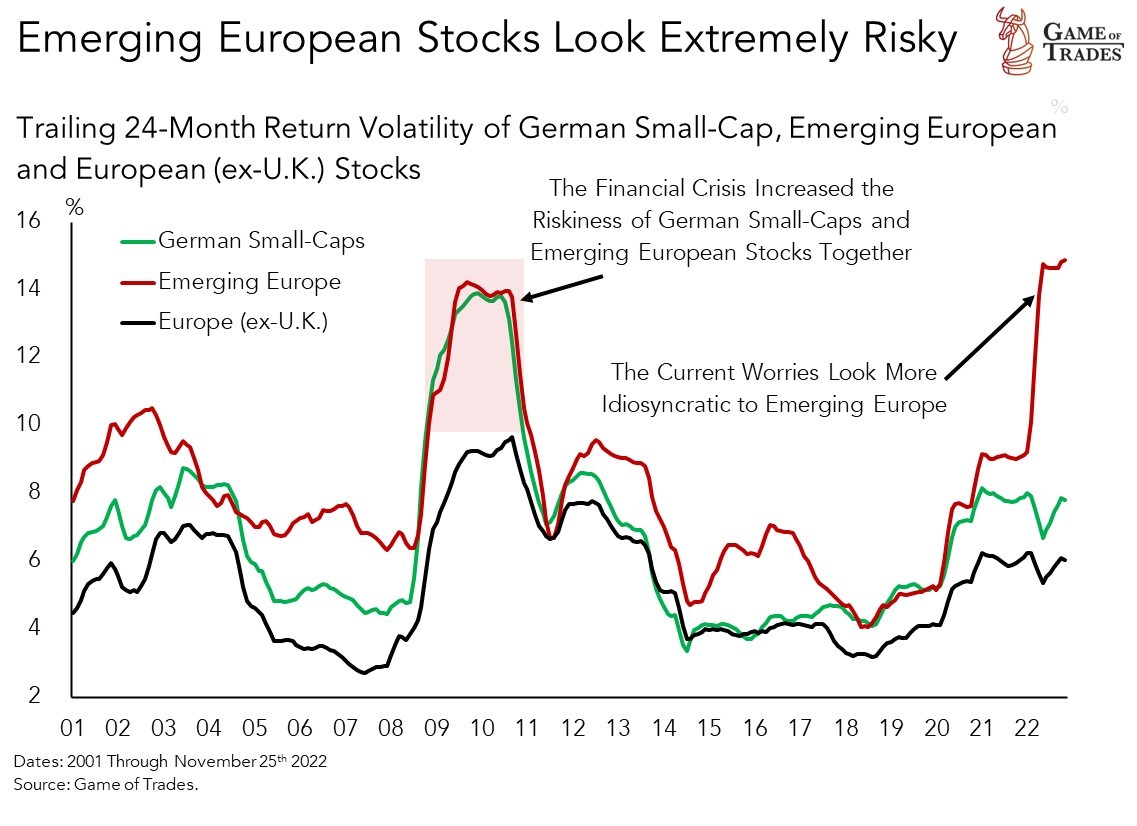

We see emerging European stocks as a similar but much riskier proposition on a resolution to the energy crisis. The huge rise in the volatility of emerging European equities this year is telling of significant idiosyncratic risk facing emerging European businesses, as shown below. While the valuations of emerging European equities look extremely cheap, the risks inherent in that bet look outsized. Moreover, we’re not looking to add more risk to our European exposure today considering our current allocation to German small-caps. For investors with a higher degree of risk tolerance, emerging European equities could prove a highly-levered opportunity to bet on a resolution to the energy crisis.

Following our analysis on emerging Europe, we’ll now turn our attention to Korea and Chinese stocks.

Korean Stocks: The Optimal Play on China’s Reopening

Chinese authorities have long used credit as a way to simulate the economy and achieve their GDP growth targets. One way of capturing the flow of credit in the Chinese economy is through the credit impulse. The credit impulse is simply the change in new credit being injected in the real economy (i.e., change in the flow of credit). When China’s credit impulse is accelerating, that means that there’s a concerted effort by the Chinese authorities to stimulate demand.

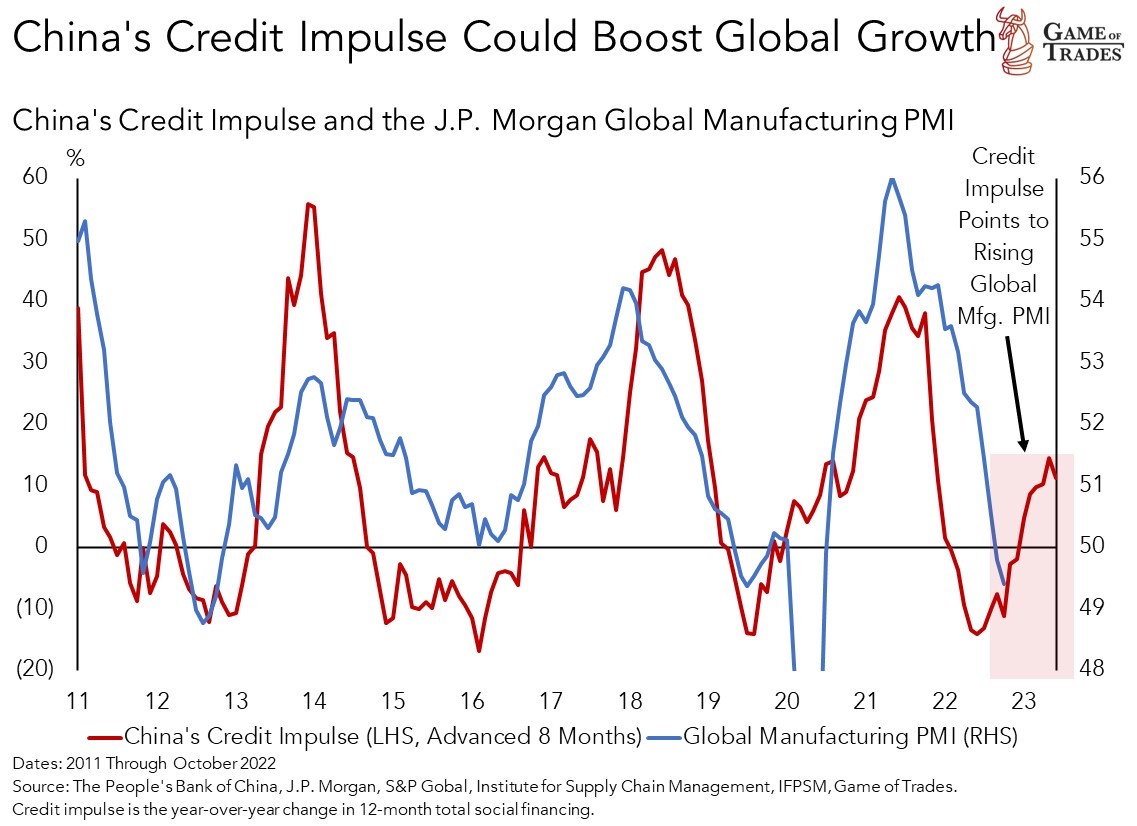

China is a big driver of the global business cycle through its credit impulse. We can see that in the chart below that compares the credit impulse with the global manufacturing PMI. We found that China’s credit impulse tends to lead global economic growth by about 8 months. When China injects liquidity into the real economy, there are positive spillover effects in the rest of the world due to a pickup in Chinese demand. Of note, the recent rise in the credit impulse implies a pickup in global growth in the next year. Of course that’s dependent on China’s ability to power through its reopening efforts amidst rising Covid cases. A successful reopening would go a long way in offsetting concerns around an upcoming hit to the global economy from the global monetary policy tightening cycle of 2022.

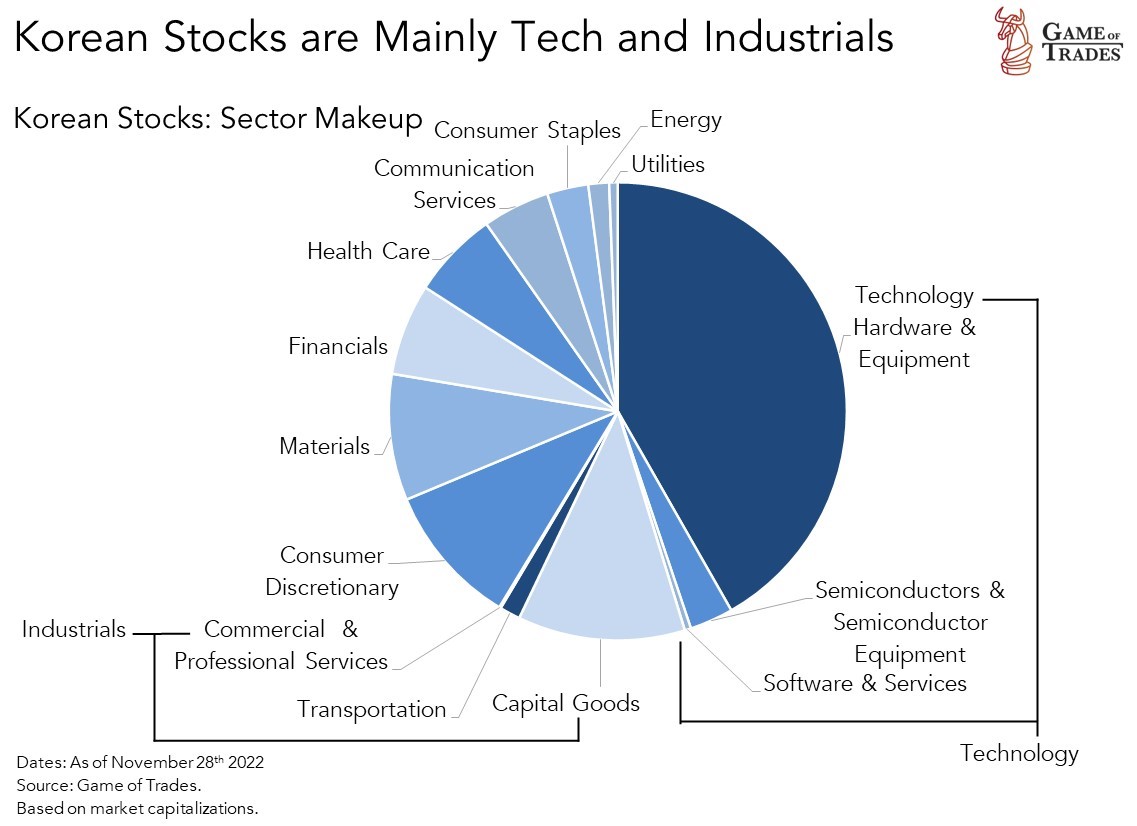

Korean stocks tend to benefit from a pick-up in global growth. Korean publicly-traded businesses are big exporters, and therefore are significantly exposed to the global economic cycle. The pie chart below documents the sector exposure of Korean publicly-traded companies. A big chunk of that market is comprised of cyclicals like semiconductor and industrial businesses, comprising over half of the total market capitalization.

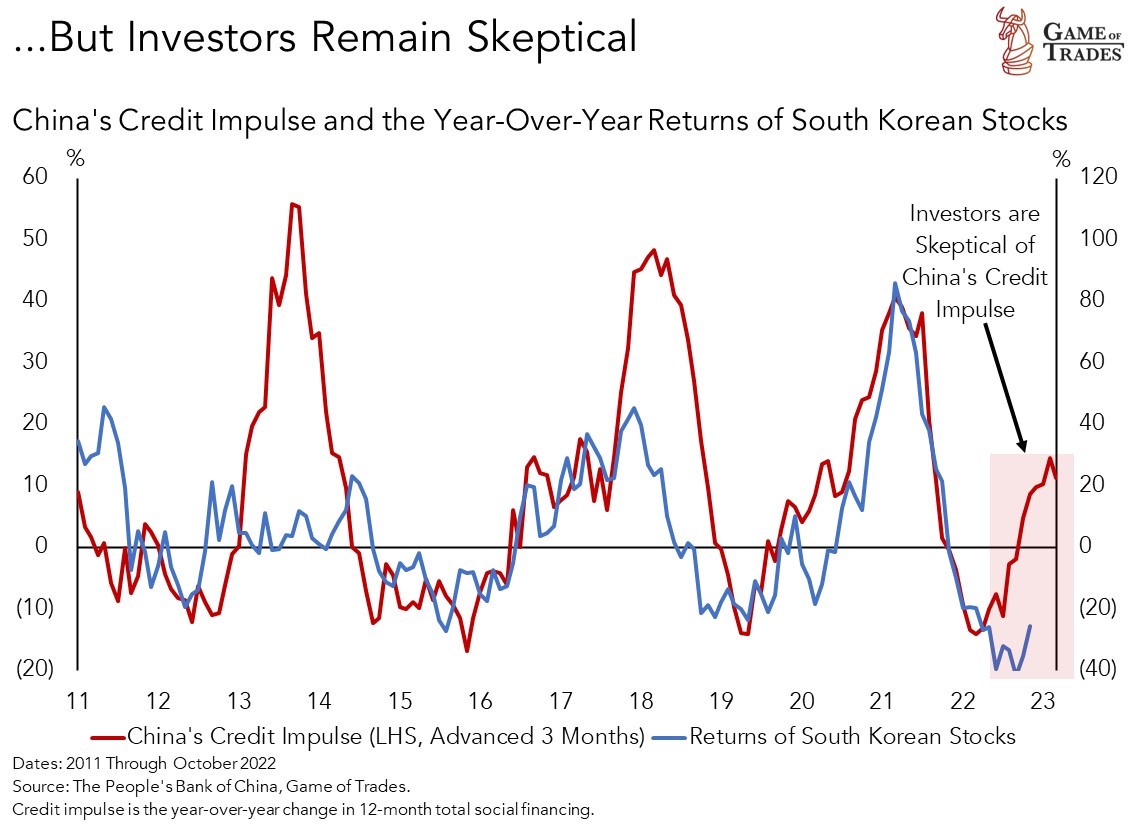

With China a big driver of the global economic cycle, what happens in China doesn’t stay in China. In fact, it spills over to Korean stocks in a big way. The chart below presents the relationship between the returns of Korean stocks and China’s credit impulse. We found that the credit impulse leads Korean stock returns by about a quarter. Of note, there’s a sizeable divergence between the two series lately. The lack of follow-through from Korean stocks to the rising credit impulse is a sign that investors are skeptical that China’s efforts to inject credit into its economy will help kickstart global growth. That’s due to the lack of demand for credit by businesses and consumers today due to the authorities’ strict Covid restrictions.

Conclusion: Adding Korean Stocks to Our Model Portfolio

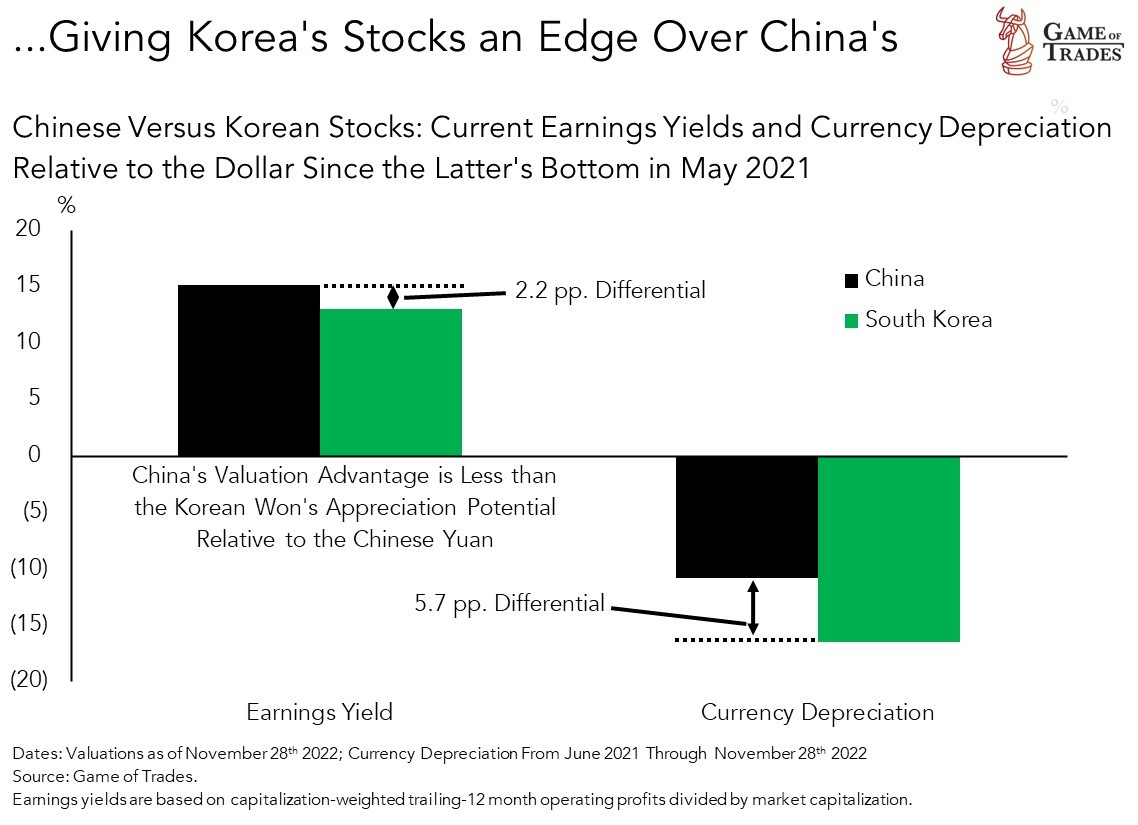

Putting everything together, we believe that Korean stocks offer the best combination of currency upside and attractive valuations in the emerging markets. The stocks are a bet on China’s economic reopening, much like Chinese equities. That said, we believe the bet to be more favorable toward Korean stocks.

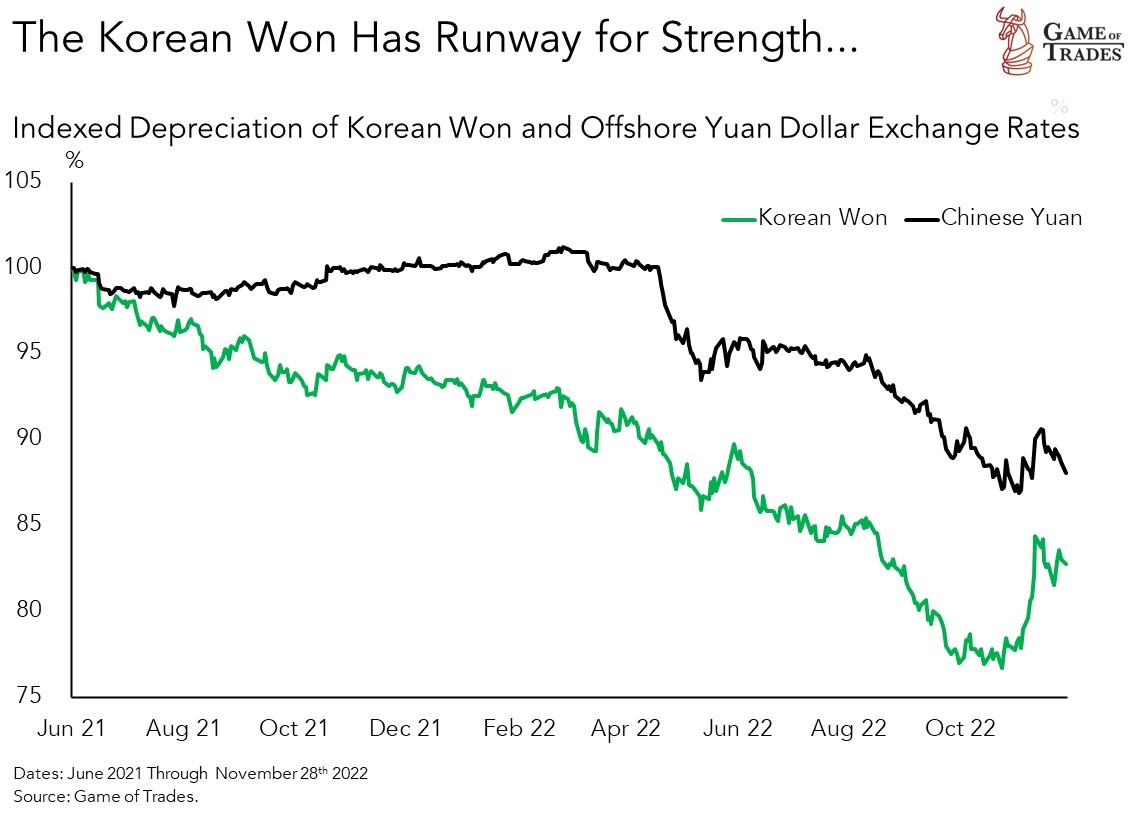

Their advantage lies in a bigger runway for the Korean won to appreciate relative to the dollar. Over the recent episode of dollar strength that began in June of last year, the Korean won has depreciated about 17% relative to the dollar. In the case of the Chinese yuan, the equivalent devaluation is about 12%. The 5 percentage point differential is a sizeable gap in currency markets.

While Chinese stocks do offer a 2 percentage points earnings yield advantage relative to Korean ones, that’s more than offset by a greater potential for the Korean won to appreciate in the next year relative to the Chinese yuan. As shown in the chart below and highlighted earlier, the Korean won’s depreciation relative to the dollar exceeded the Chinese yuan’s by over 5 percentage points since the beginning of the greenback’s upcycle that began in June of 2021.

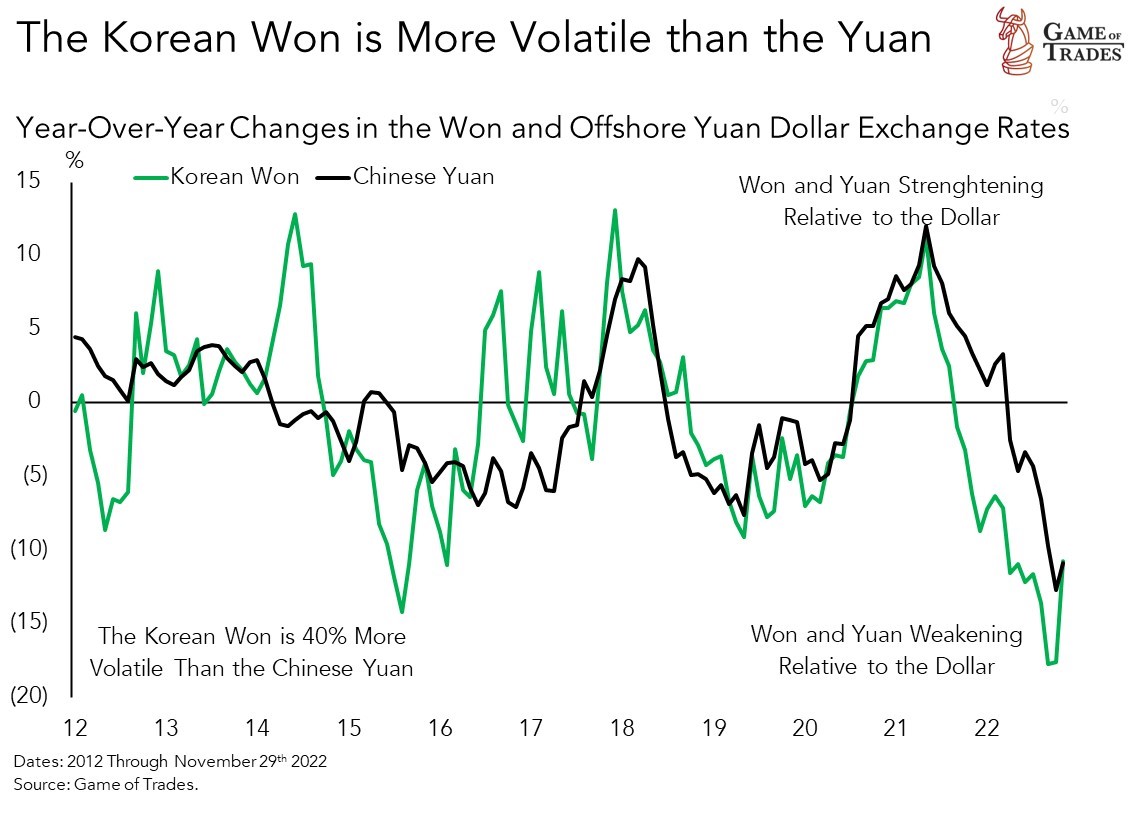

That means the potential boost to Korean stocks from a weakening dollar is greater than we can expect for Chinese ones. That’s due to the Korean won’s higher volatility relative to the Chinese yuan, as the latter is managed by the Chinese central bank. That’s shown in the chart below that compares the year-over-year changes in both currencies. We can see that the Korean won tends to fluctuate around the more stable yuan.

The table below documents the addition of the Korean ETF EWY to our model portfolio. We’re adding a 5% allocation to match that of German small-caps. Combining these two bets with our copper miners brings the non-U.S. allocation to around 17% of the portfolio. That makes for close to a 70%/30% split between U.S. and non-U.S. stocks, a good balance.

To fund our new allocation to Korean stocks we’re trimming our U.S. equity sector exposures. We’re taking down the weight of consumer discretionary (XLY), technology (XLK) and transportation (IYT) by 2, 1.5. and 1.5 percentage points, respectively. Those changes are documented in the table below.

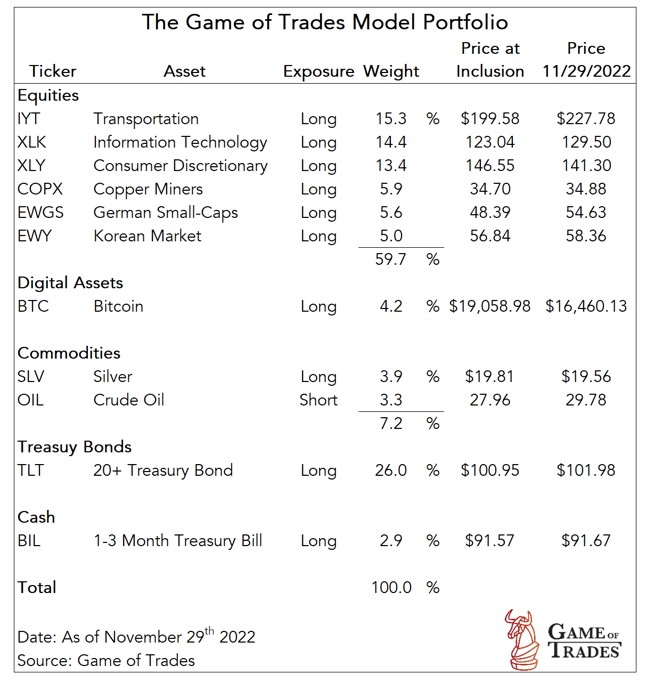

The updated portfolio is shown in the table below. The biggest exposure remains to U.S. equities. As we’ve documented in our work, the bet there is on peaking U.S. interest rates driven by waning inflation pressures. We believe that outcome will drive equity market valuations higher, with transportation, tech and consumer discretionary stocks our picks. Our sizeable allocation to long Treasury bonds provides a hedge in the event the economy deteriorates more than we expect.

We’re also betting on a weakening dollar. We believe that’ll be driven by a reopening of the Chinese economy, bringing U.S. rate differentials with China lower. We also expect the pessimism surrounding the energy crisis in Europe to recede, putting downside pressure on the dollar. Both events would bring about more certainty in the global economy, reducing the appeal of holding dollars. We’re expressing that idea through copper miners, German small-caps, Korean stocks, Bitcoin and silver.

Footnotes

[1] We assume that U.S.-based investors are not hedging the currency risk in their holdings of foreign stocks.

[2] Local currency returns are the returns experienced by local investors (i.e., Chinese investors holding Chinese stocks). U.S.-based investors don’t earn local currency returns as they have to convert their dollars to foreign currency to buy foreign stocks. Rather, they earn dollar-based returns, as following the closing of their foreign stock positions they have to convert the proceeds earned in foreign currency back to U.S. dollars. If the foreign currency appreciates while the stocks are being held, then that appreciation adds to the returns earned by U.S.-based investors, and vice-versa.

[3] We use the earnings yield, as opposed to the P/E ratio, to incorporate negative earnings. The P/E ratio omits negative earnings and hence can provide a biased assessment when evaluating companies that are under significant stress.

Congratulations, you are doing a great job!

Fantastic job @GOT. The thesis is materializing.

Is anyone else having trouble with the live charts playing? (None in this article). I can’t log into trading view directly from the chart (no captcha box), and logging in with a different tab does not work. Thanks.

[…] We added Korean stocks (EWY) to our portfolio in late-November as a bet that China’s removal of Zero Covid policies would stimulate global growth and our expectations of a weakening dollar. […]

[…] Korean stocks exposure of 4.8% through EWY remains as is for now. The ETF is a derivative of China reopening. We’ll revisit our view on China later this […]