Key Developments

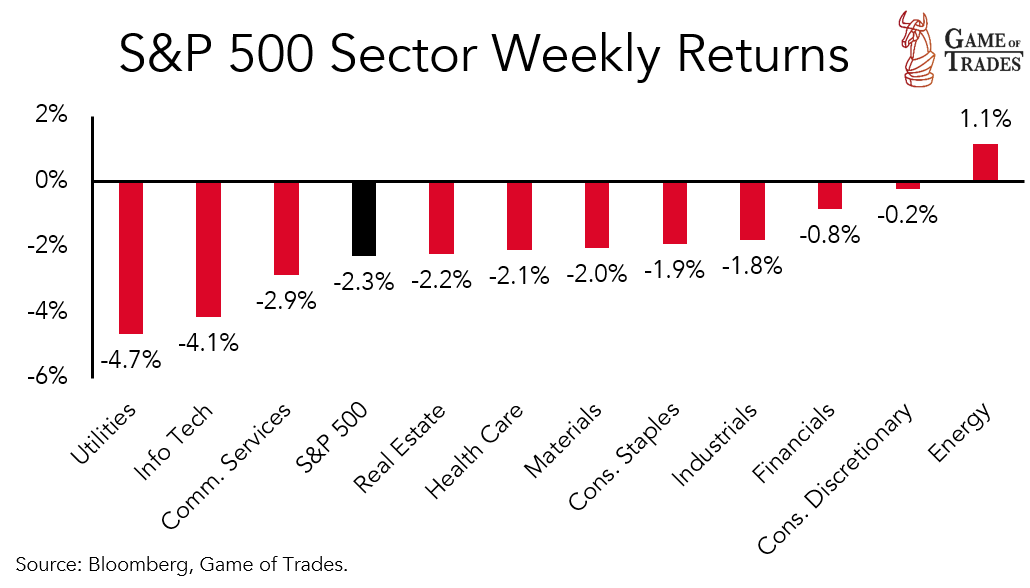

- The S&P 500 declined 2.3%, the worst weekly return since March. Energy was the only sector higher, climbing 1.2%, while Tech (-4.1%) and Utilities (-4.7%) lagged.

- Q2 earnings results were mixed throughout the week, with notable mega caps AMZN beating expectations, while AAPL missed analyst estimates, which pressured the Tech sector.

- The ISM Manufacturing Index remained in contraction in the month of July, reporting at 46.4, while ISM Services stayed expansionary at 52.7.

- 10-year Treasury yields spiked, reaching as high as 4.20% Thursday before closing the week at 4.03%. News of increased Treasury issuance, the downgrade to US debt by Fitch, the shift in Japan’s yield curve control and better-than-expected economic data appeared to drive the move.

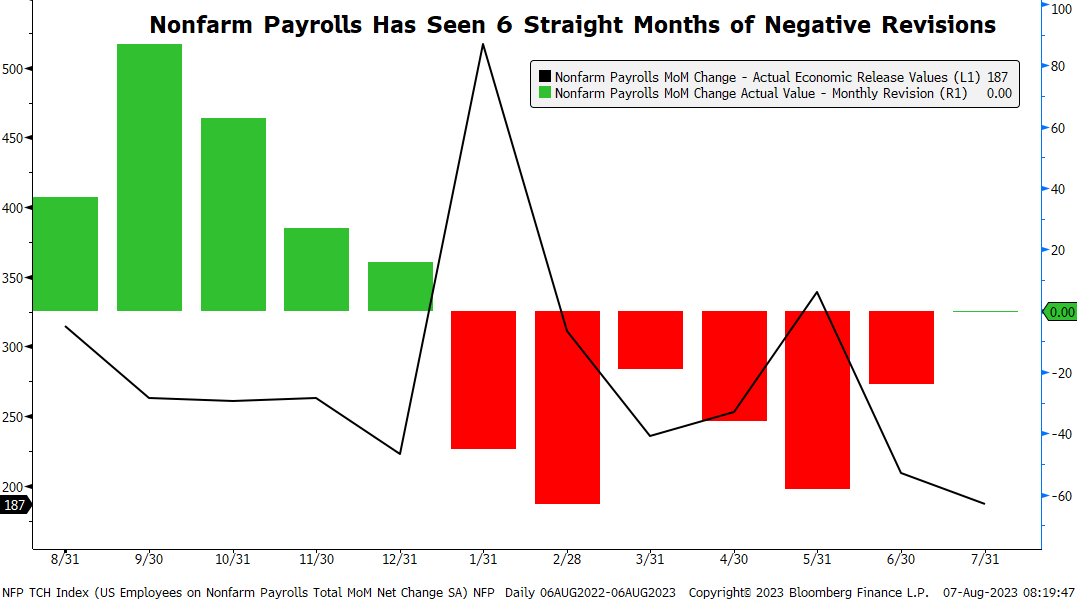

- The jobs report showed a moderation of nonfarm payrolls growth, rising 187,000 last month, below the 200,000 consensus estimate. The unemployment rate ticked lower to 3.5%.

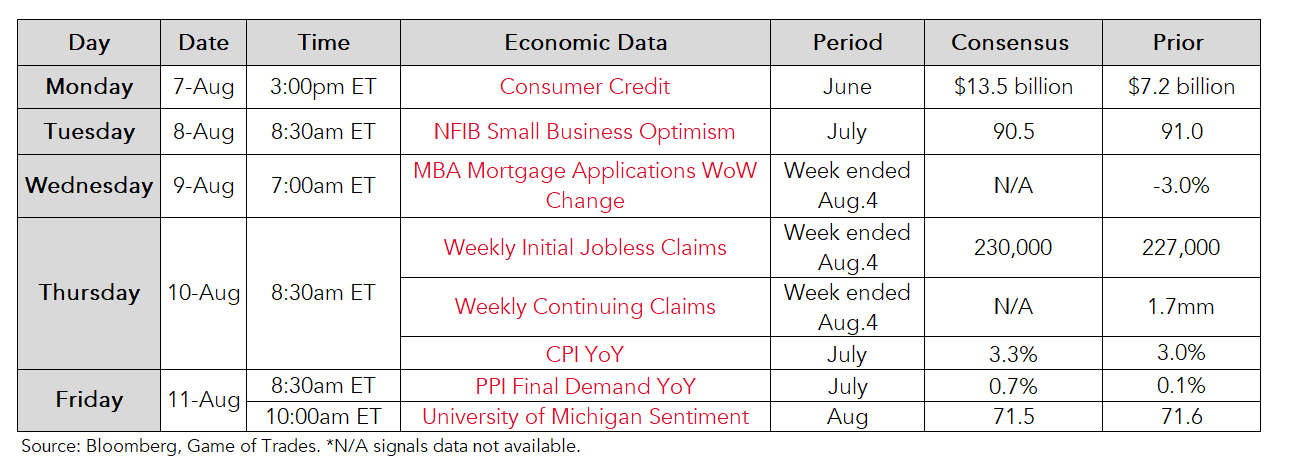

- The July CPI report on Wednesday is the key data to watch this week, with an estimate of 3.3% YoY for headline CPI.

This Week’s Economic Data

Chart of the Week

Monthly Jobs Growth Numbers Have Continued to See Negative Revisions

- For the sixth straight month, the last month’s payrolls number was revised lower versus the initial reported estimate.

- This shows a slightly less constructive labor market underneath the hood, and is something to monitor over coming months.

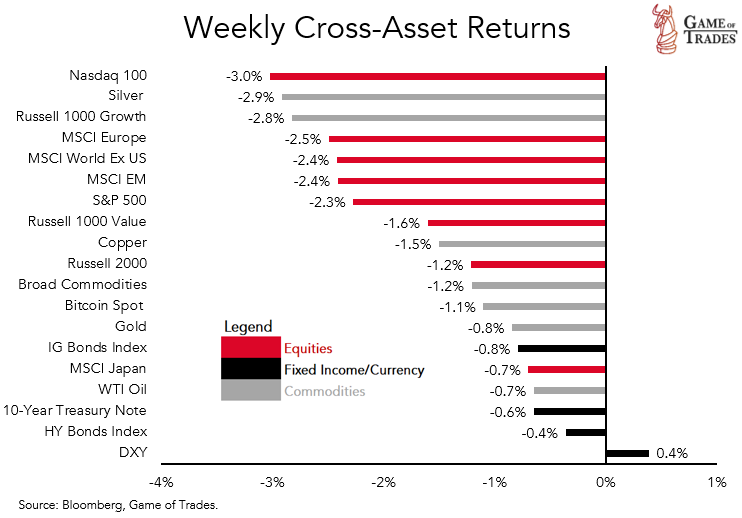

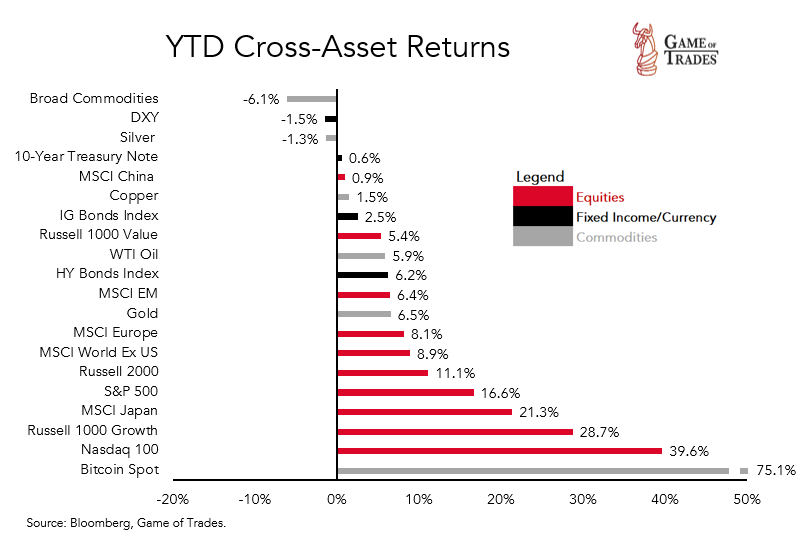

Global Cross-Asset Performance Summary

Weekly

Year to Date

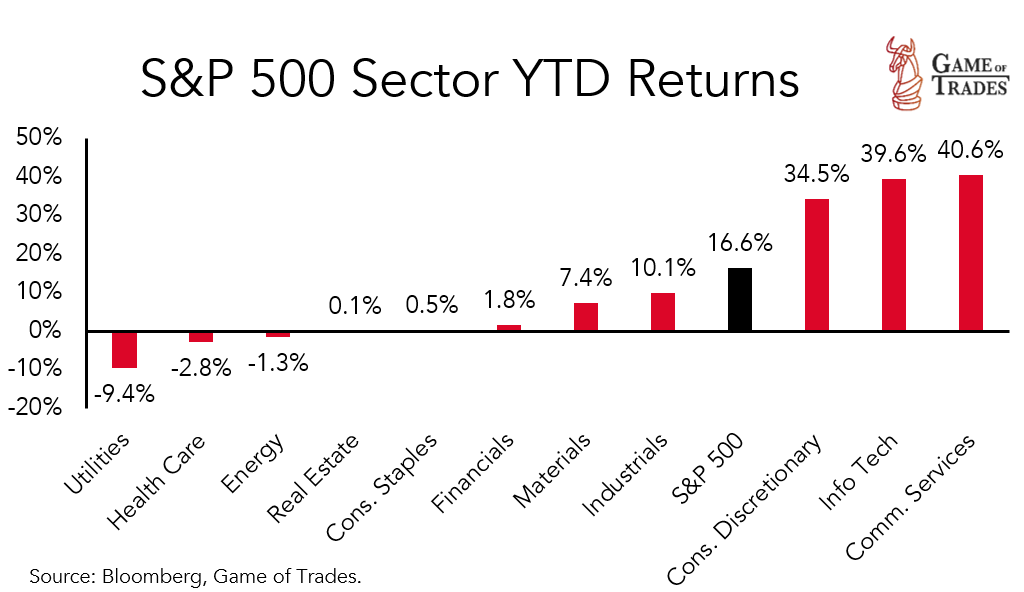

S&P 500 Sector Performance

Weekly

Year to Date

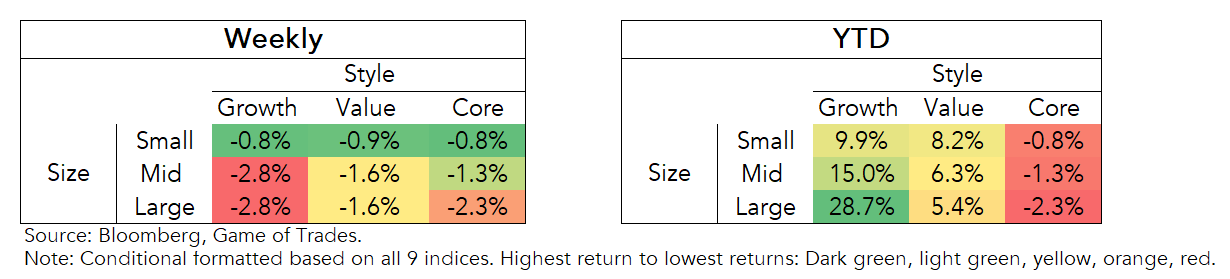

US Equity Market Style and Size Performance

these weekly roundups are very helpful for investors like me who arent that active in managing their investments. Gives a good look at the market at a glance.